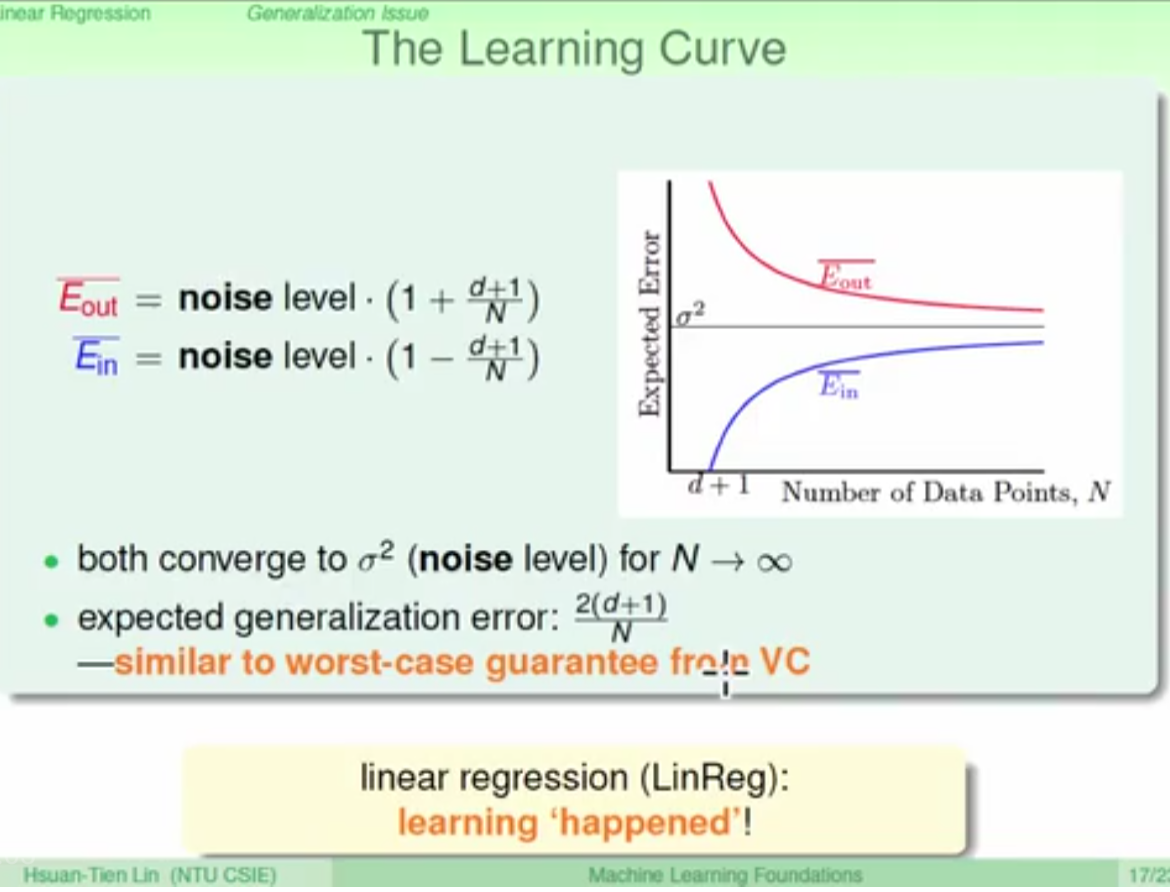

Linear regression

during linear regression, both Ein and Eout converge to sigma square, so the expected error( square error) between them is show in the pic.

d: vc dimension

N: Number of data points

logistic regression

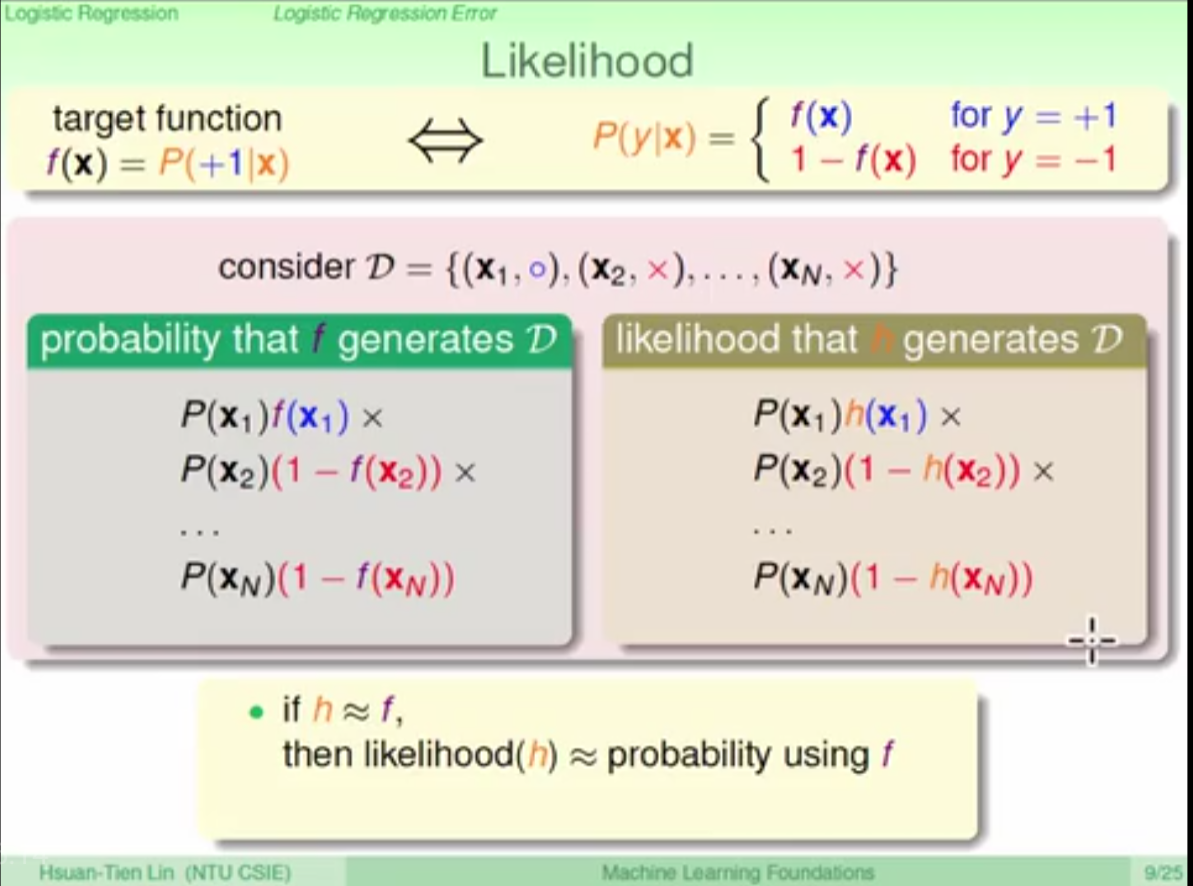

Error definition

the output of logistic regression is generated by sigmoid function

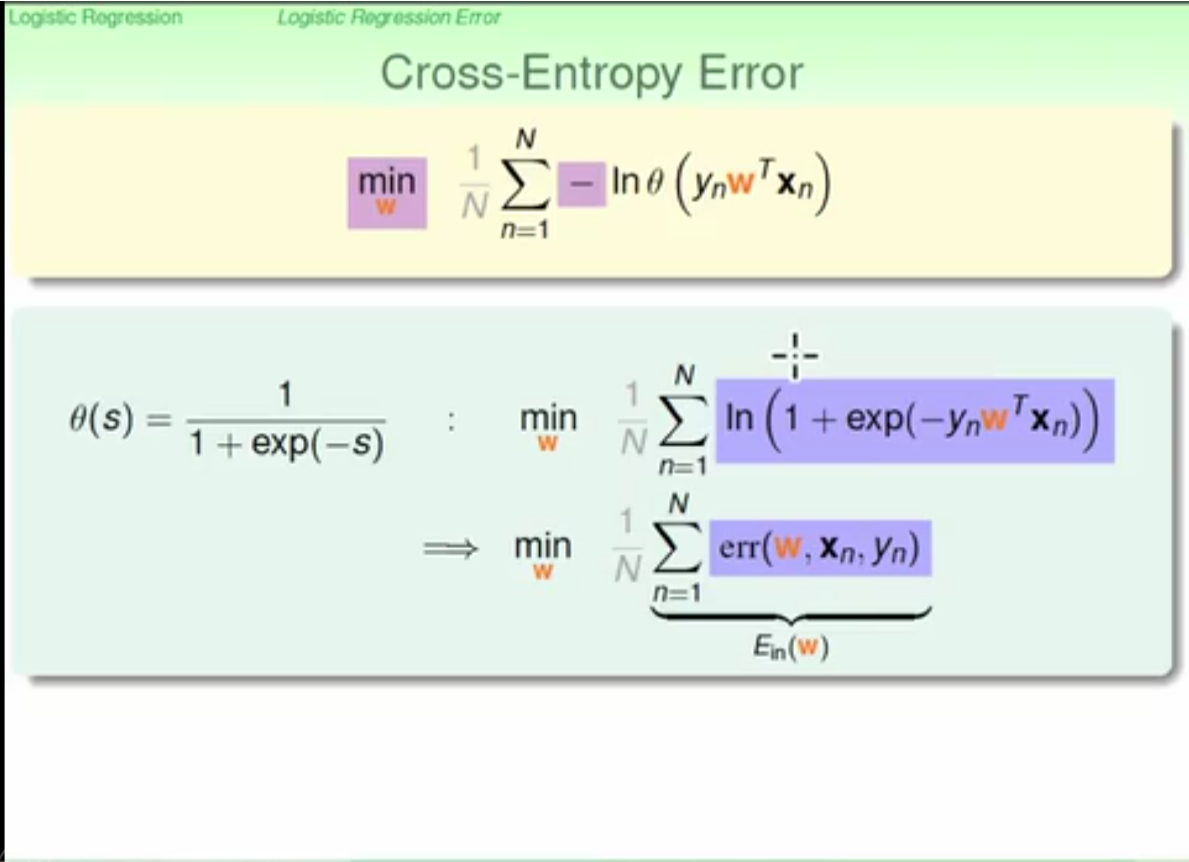

the logistic regression error is defined by maximizing the likelihood the h equal f, which is called crosss entropy error. this error is related to w, xn and yn

this is the mathmatical form of cross entropy error for calculation

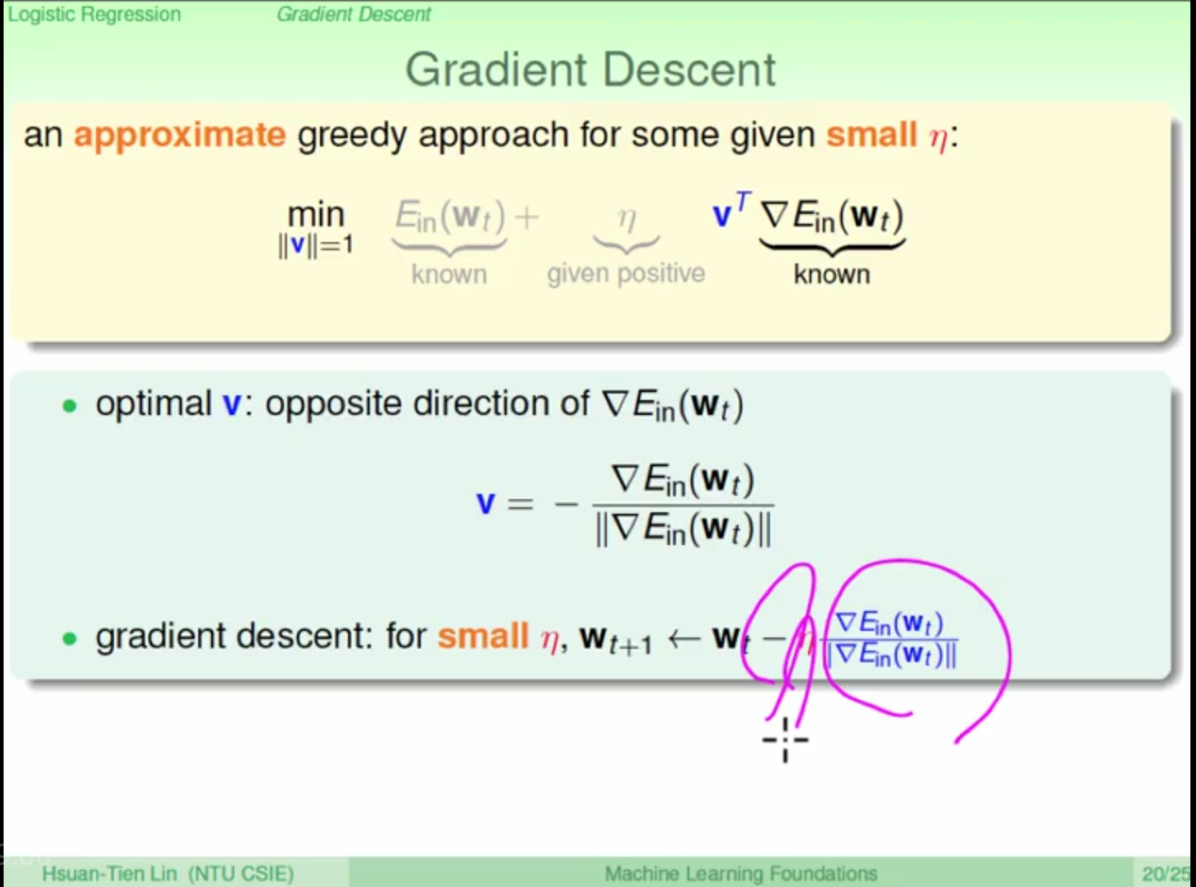

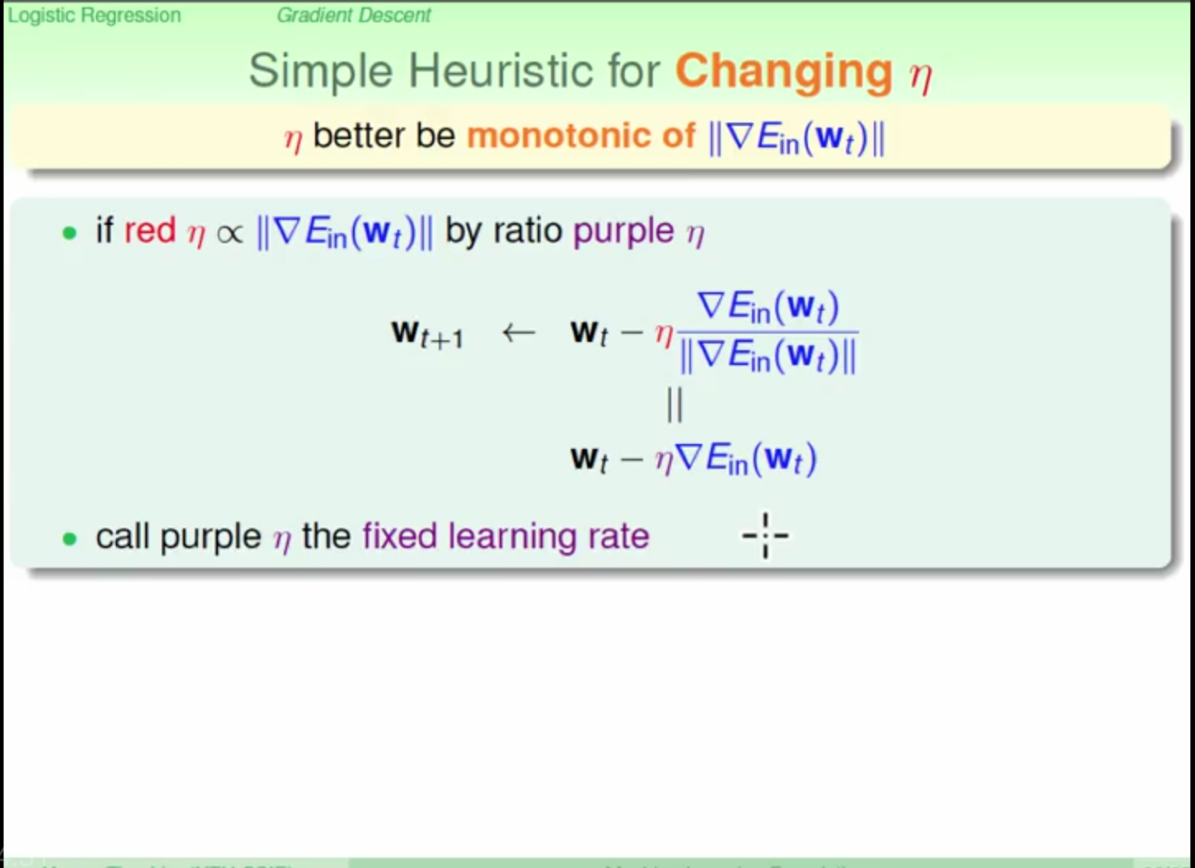

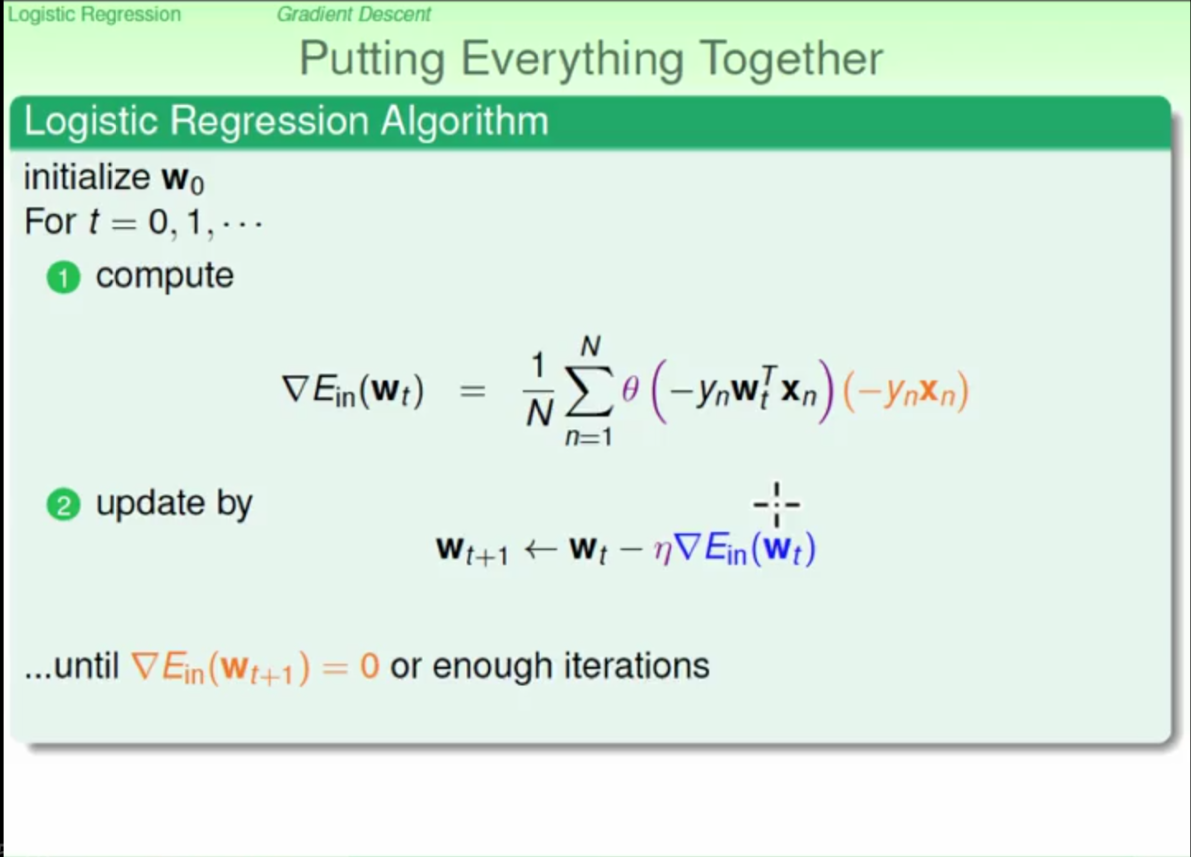

Gradient decent and learning rate

the optimal gradient descent direction is opposite direction of Delta-Ein

purple niu is teh learning rate

the training process is described in the chart

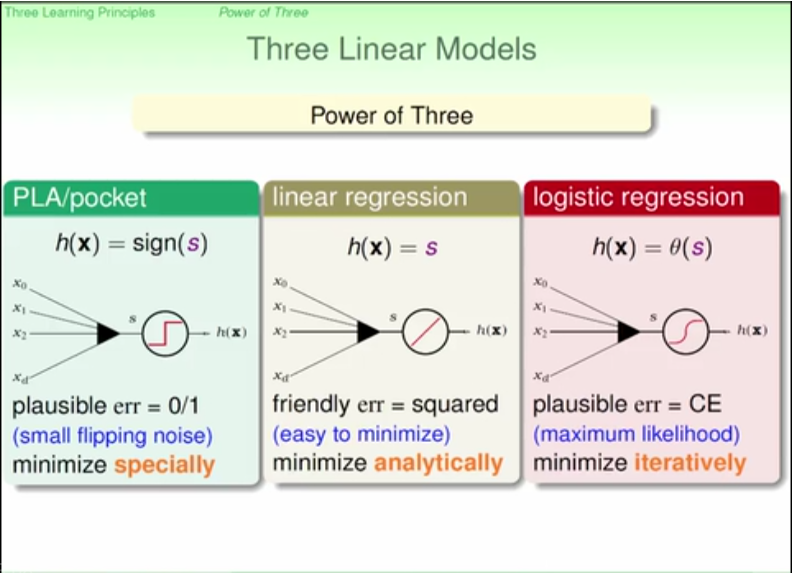

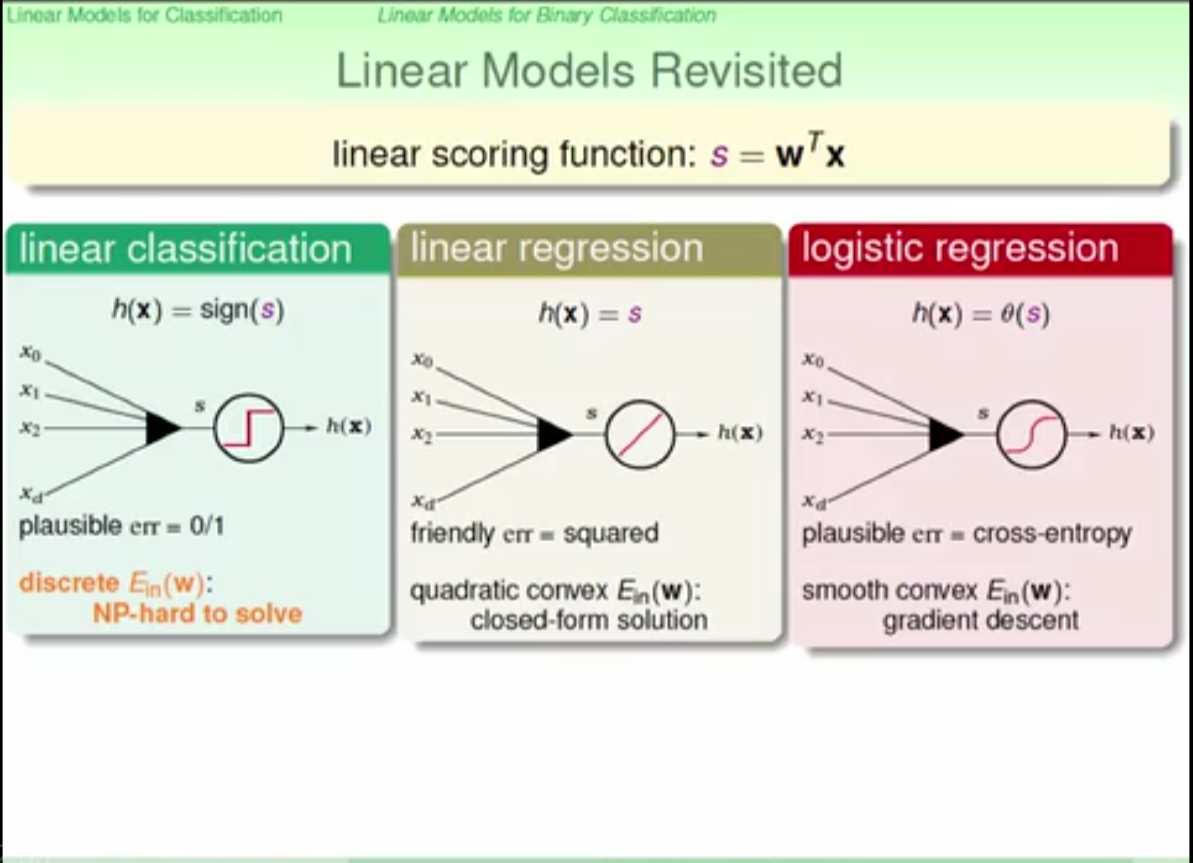

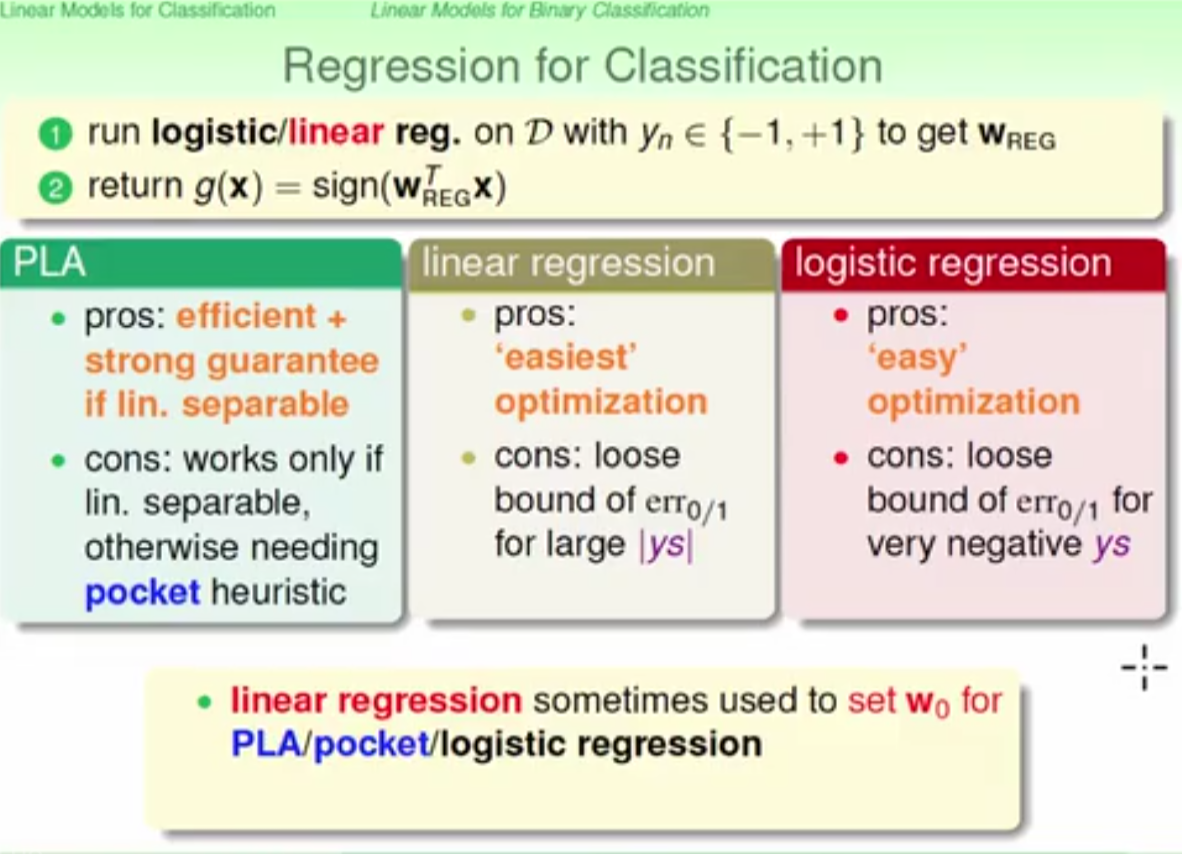

Linear model

advantages and disadvantages

demenstration of advantages and disadvantages between threee linear models

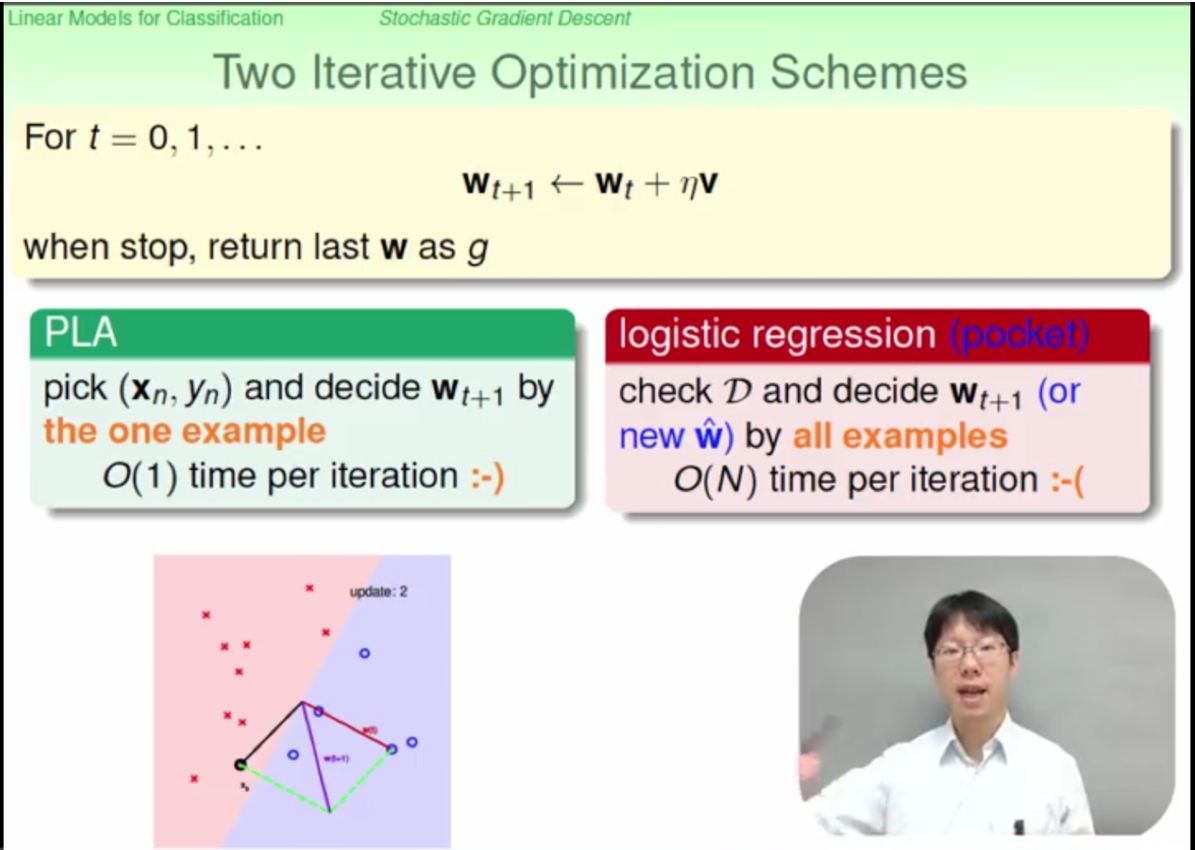

optimization process

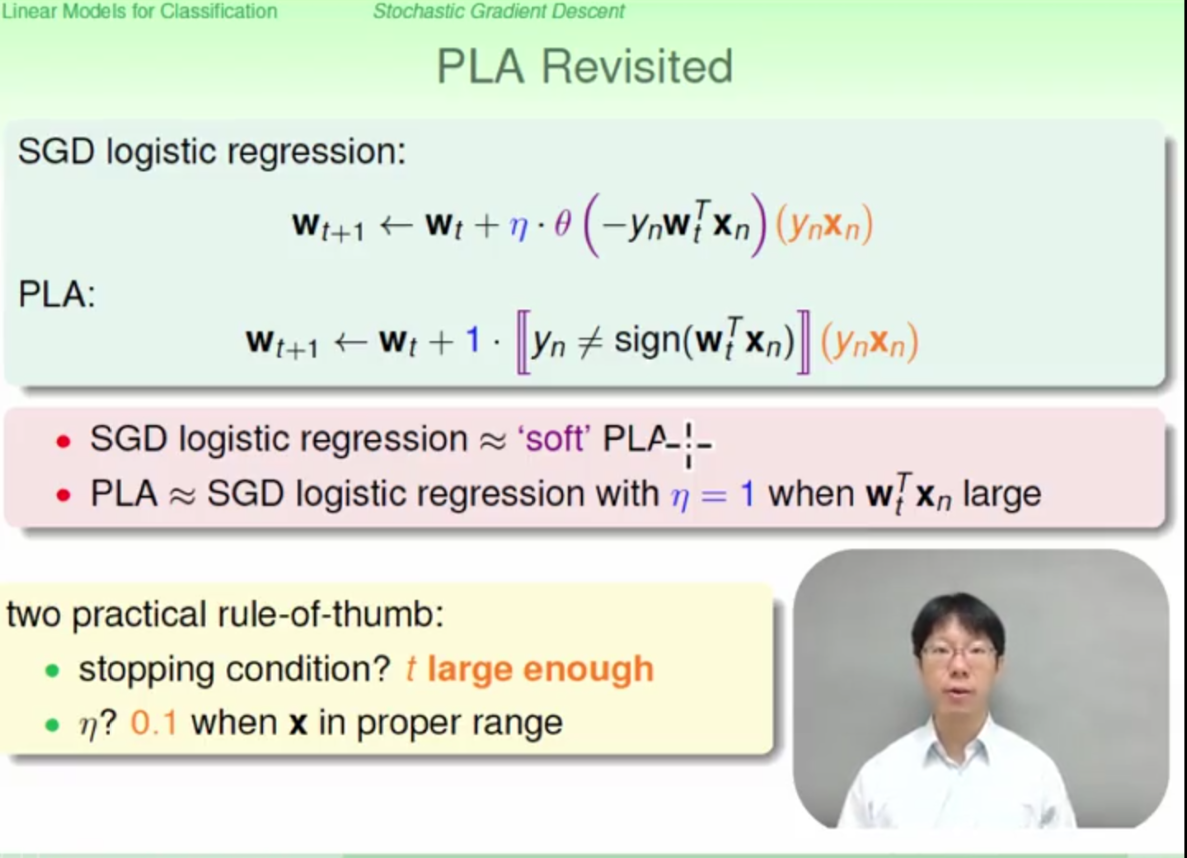

what means stochastic gradient descent??

SGD logistic regression can be seen as a softed PLA

stop criterien during training:

*iteration times

niu (learning rate )is set as 0.1(experience value)

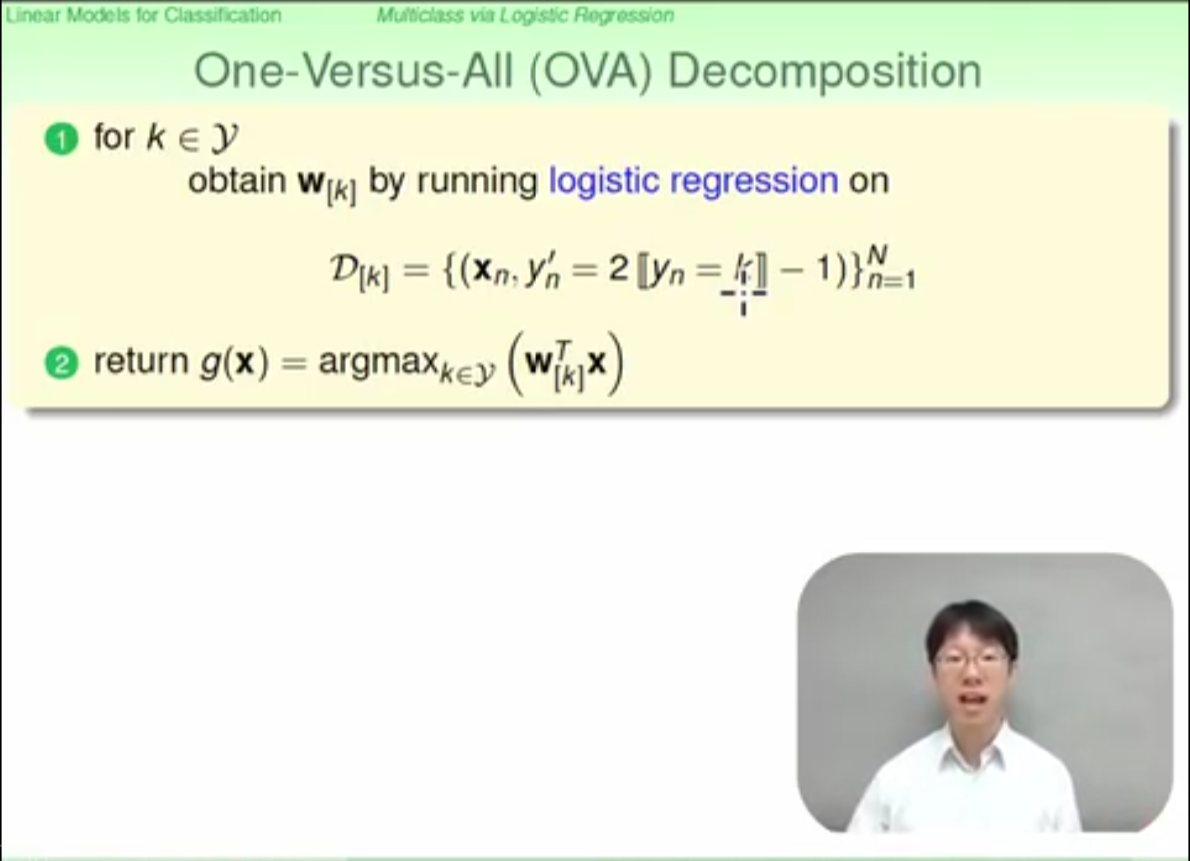

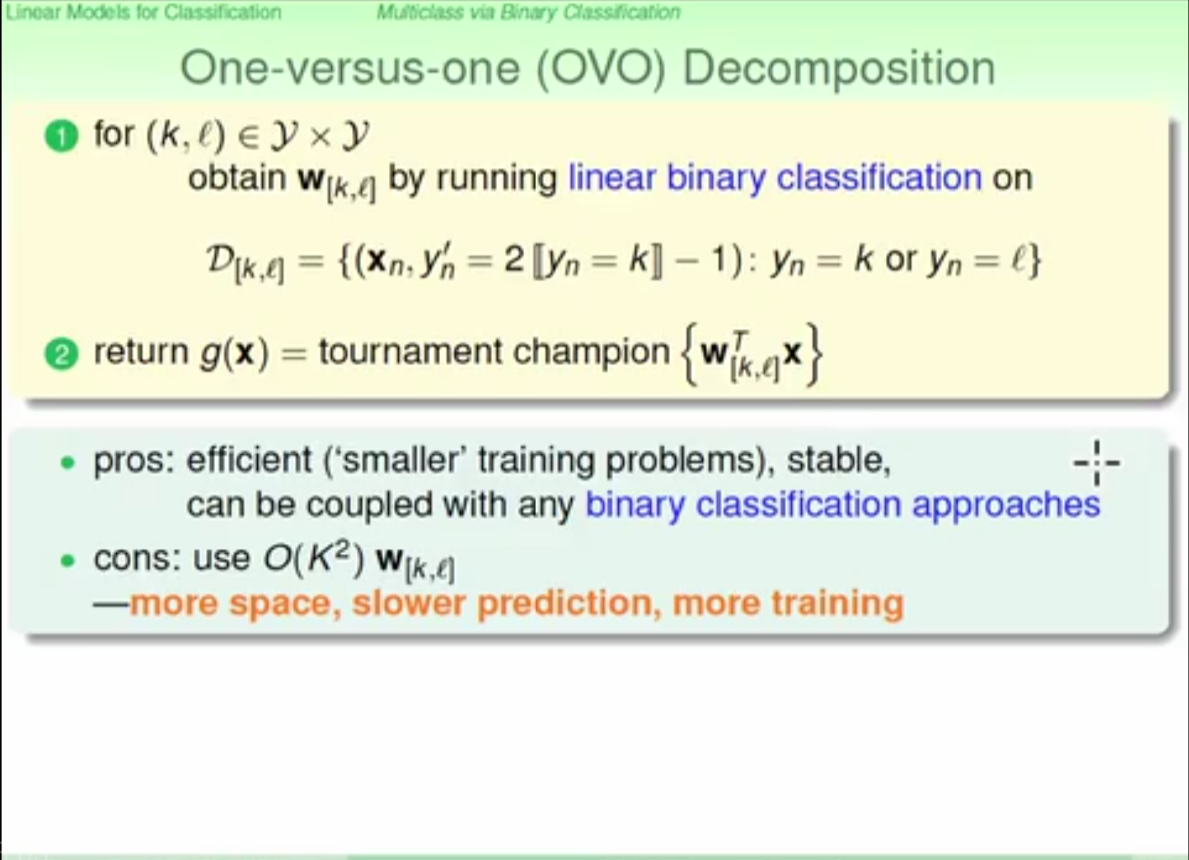

multiclass classification

two methods to deal with multiclass classification

- OVA(one versus all)[not recommended, not clearly seperatable]

- OVO(one versus one )

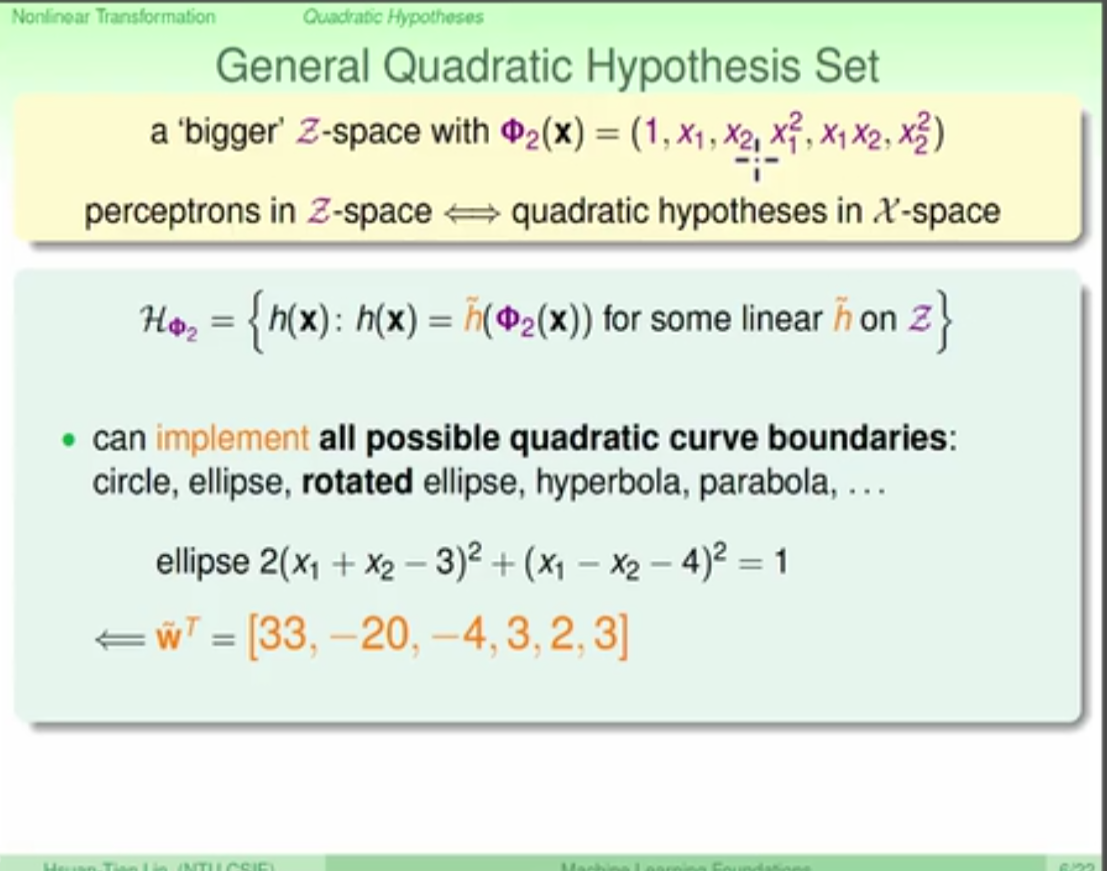

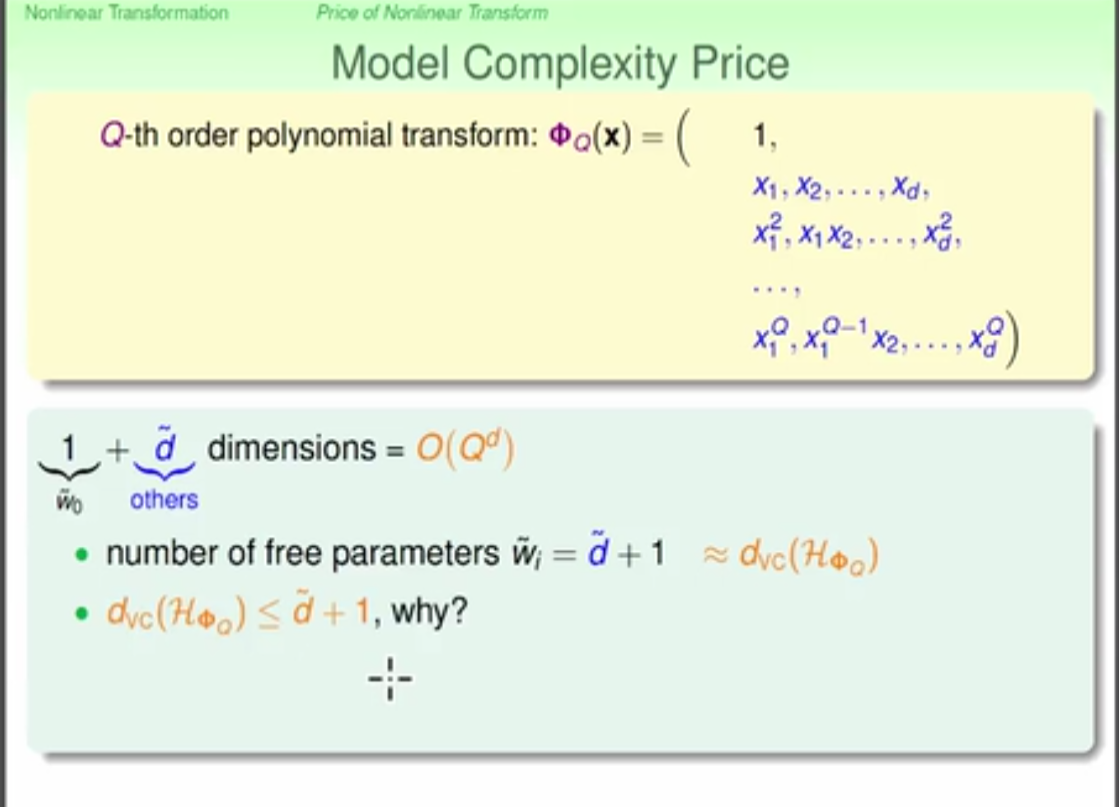

nonlinear transformation

the principle to deal with nonlinear problem is to transform the data from nonlinear space to linear space, and use linear model to deal with it. However this will lead to more complex model, so there are some parameters( C, lambda) to restrict the complexity of the model (regularization???)

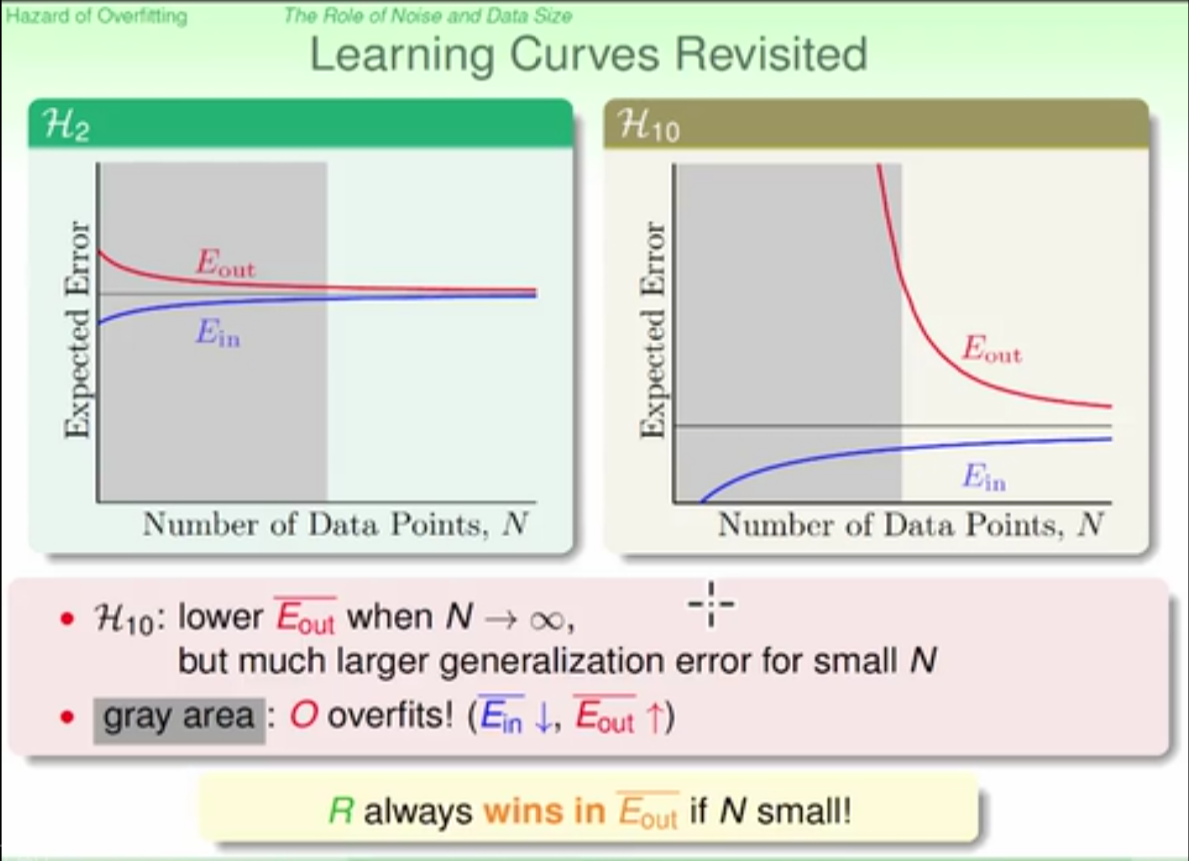

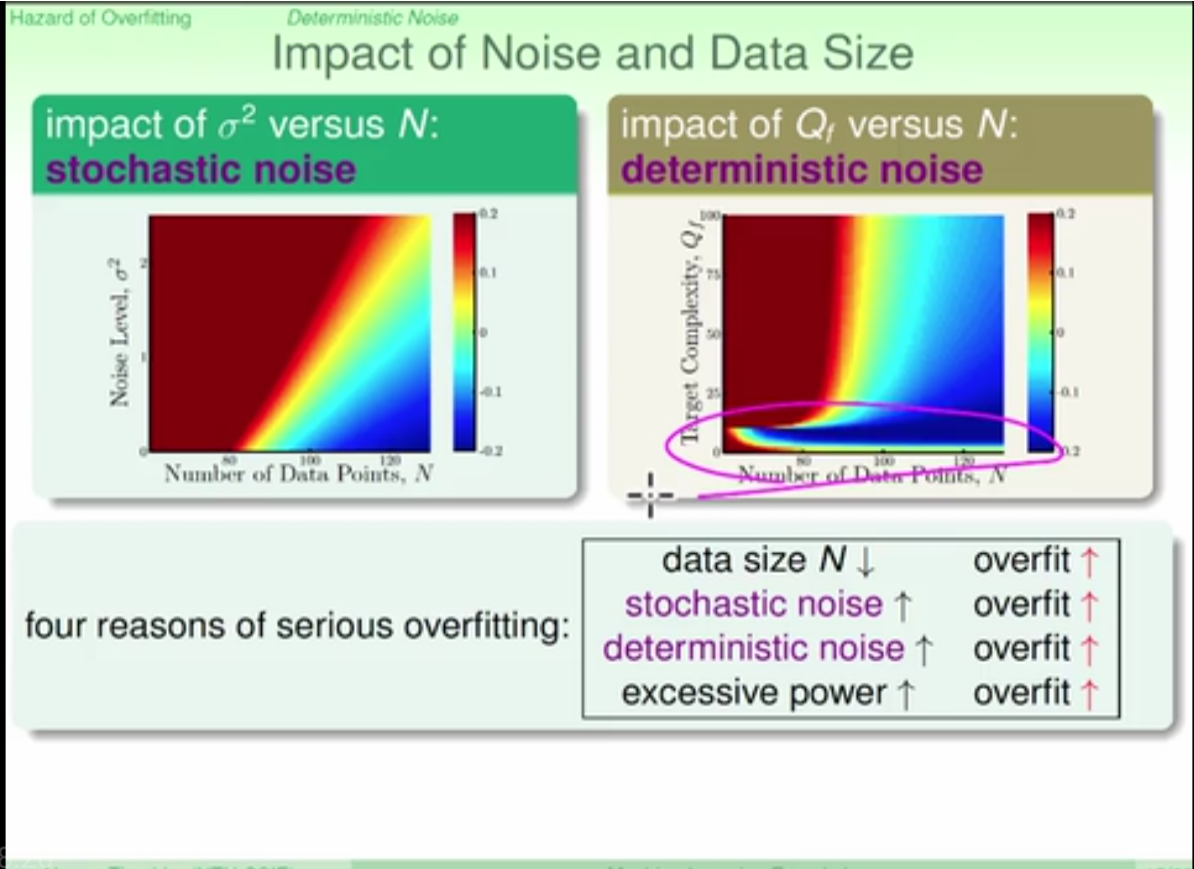

overfitting

use more complex model is not good expecially when number of data points is small

four reasons leading to oversfitting:

- data size

- stochastic noise

- deterministic noise

- excessive power (model complexity)

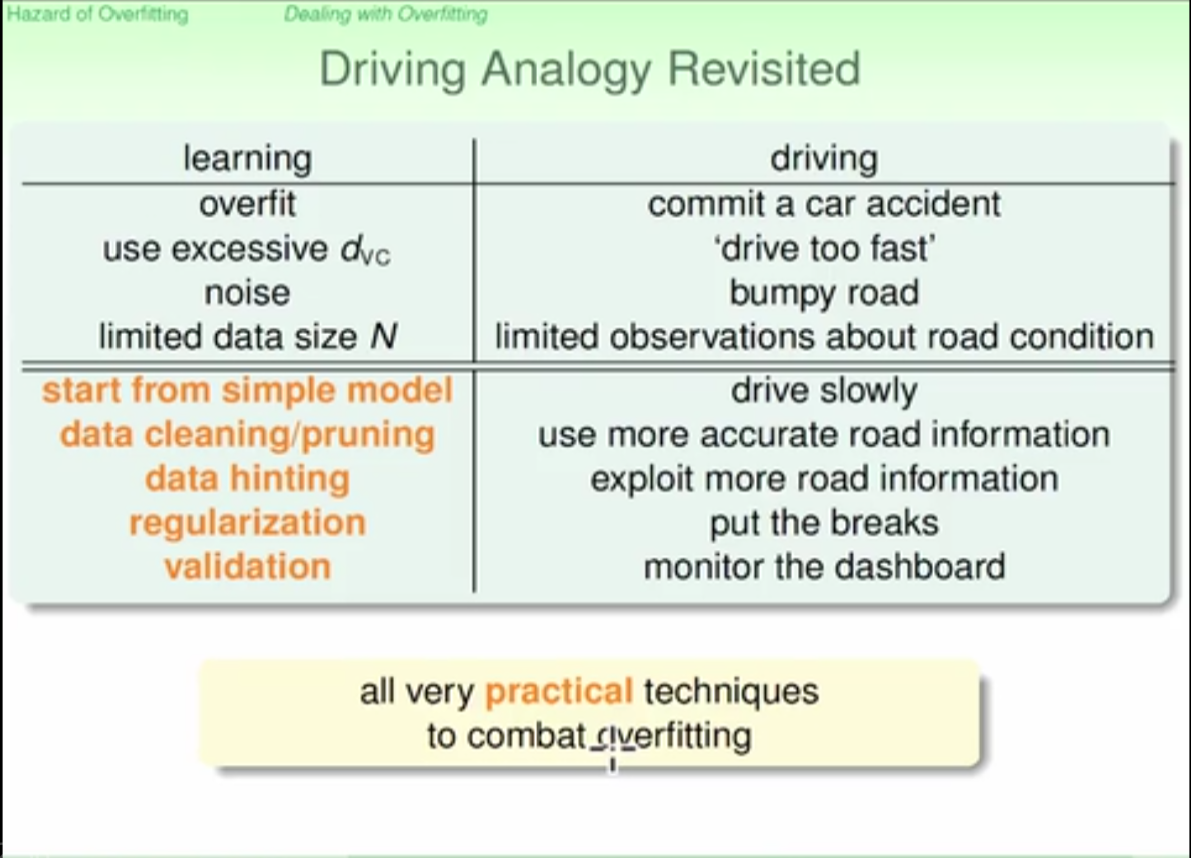

suggested ways to avoid overfitting:

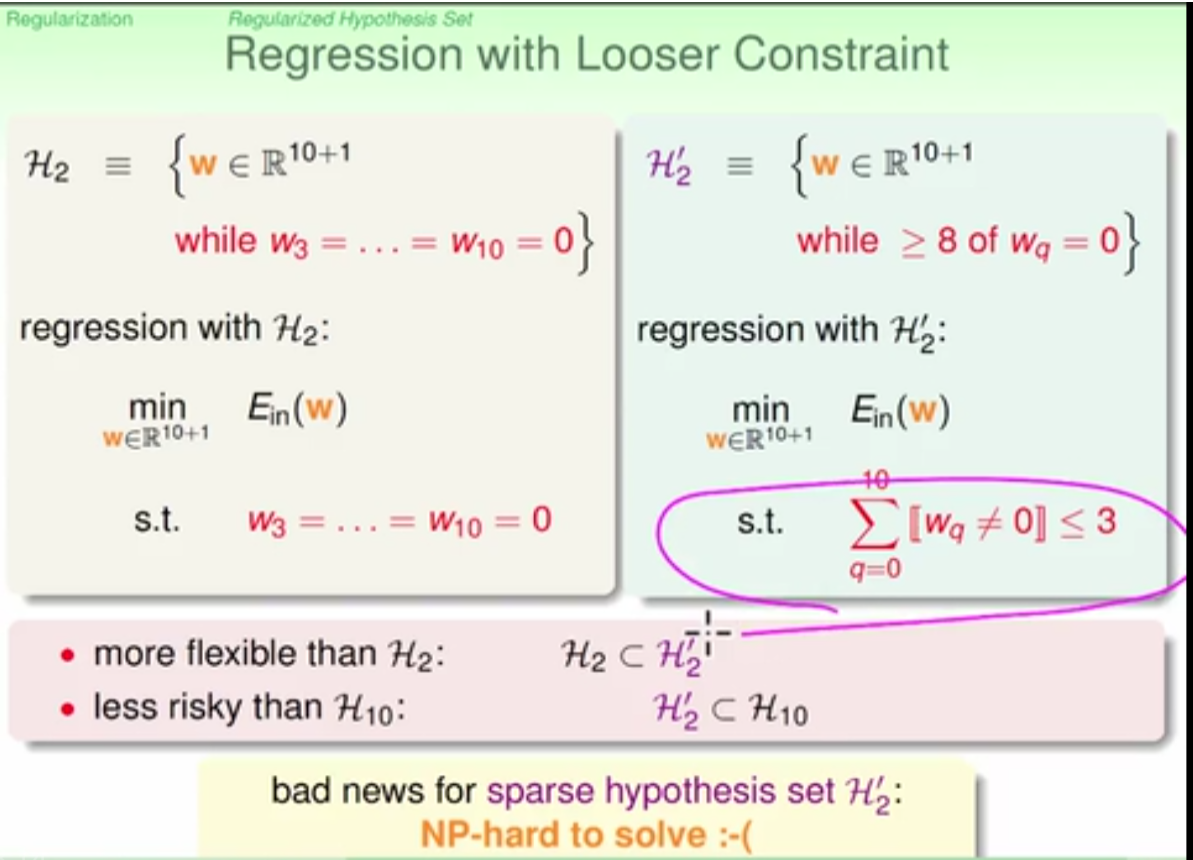

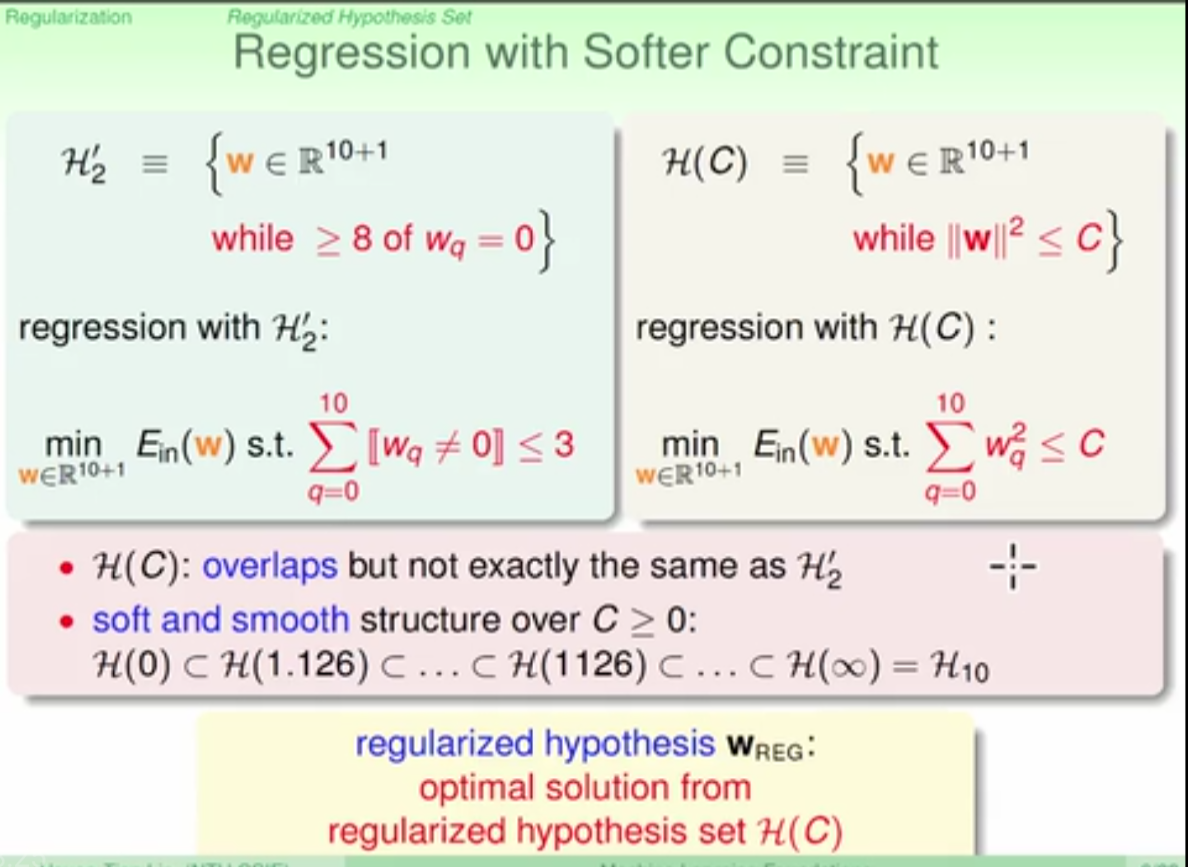

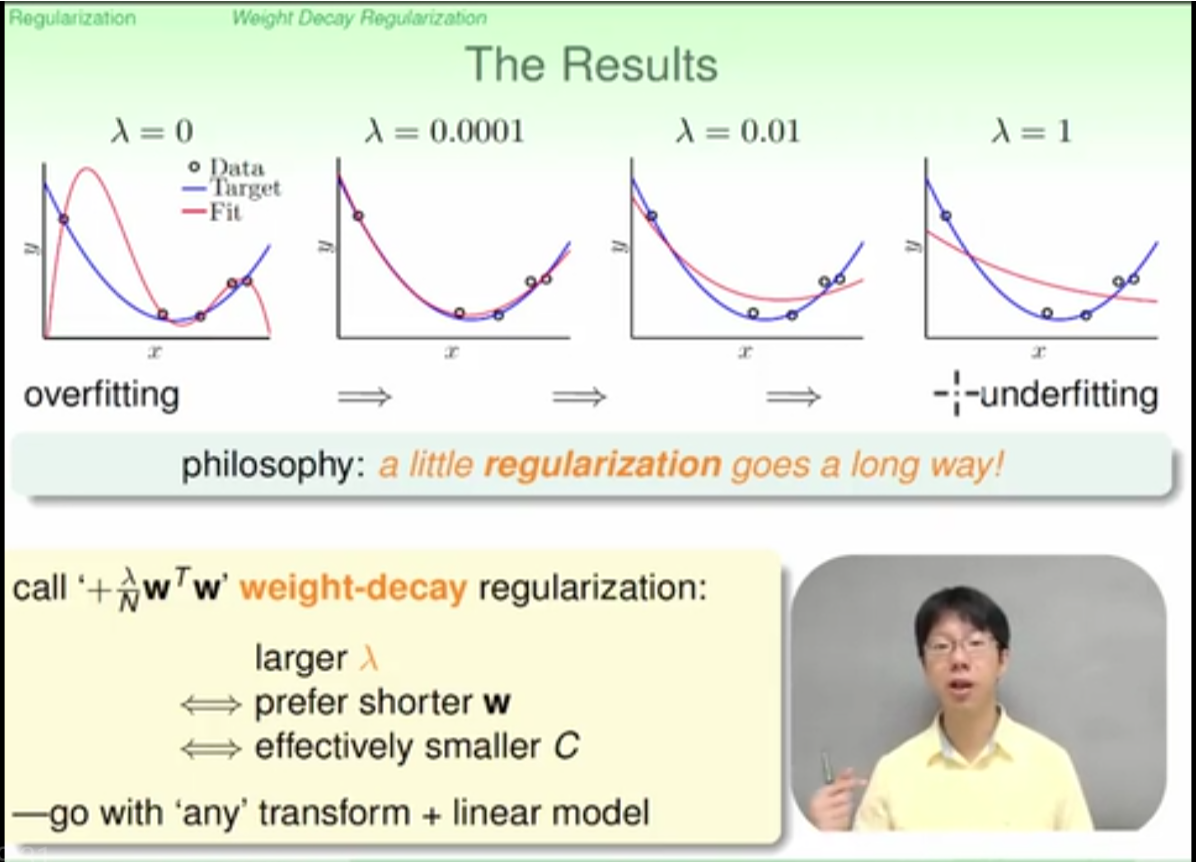

regularization

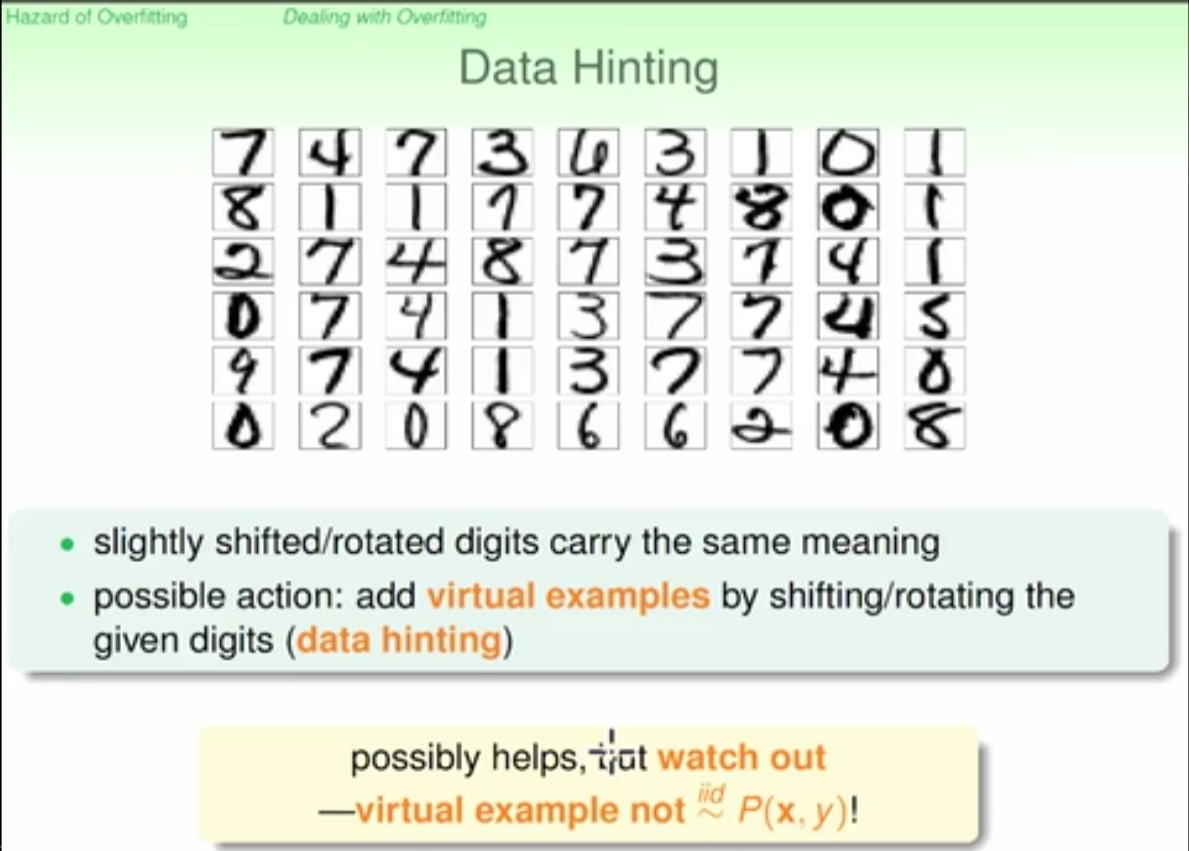

loosing and softing the constraints to deal with the nonlinear problem

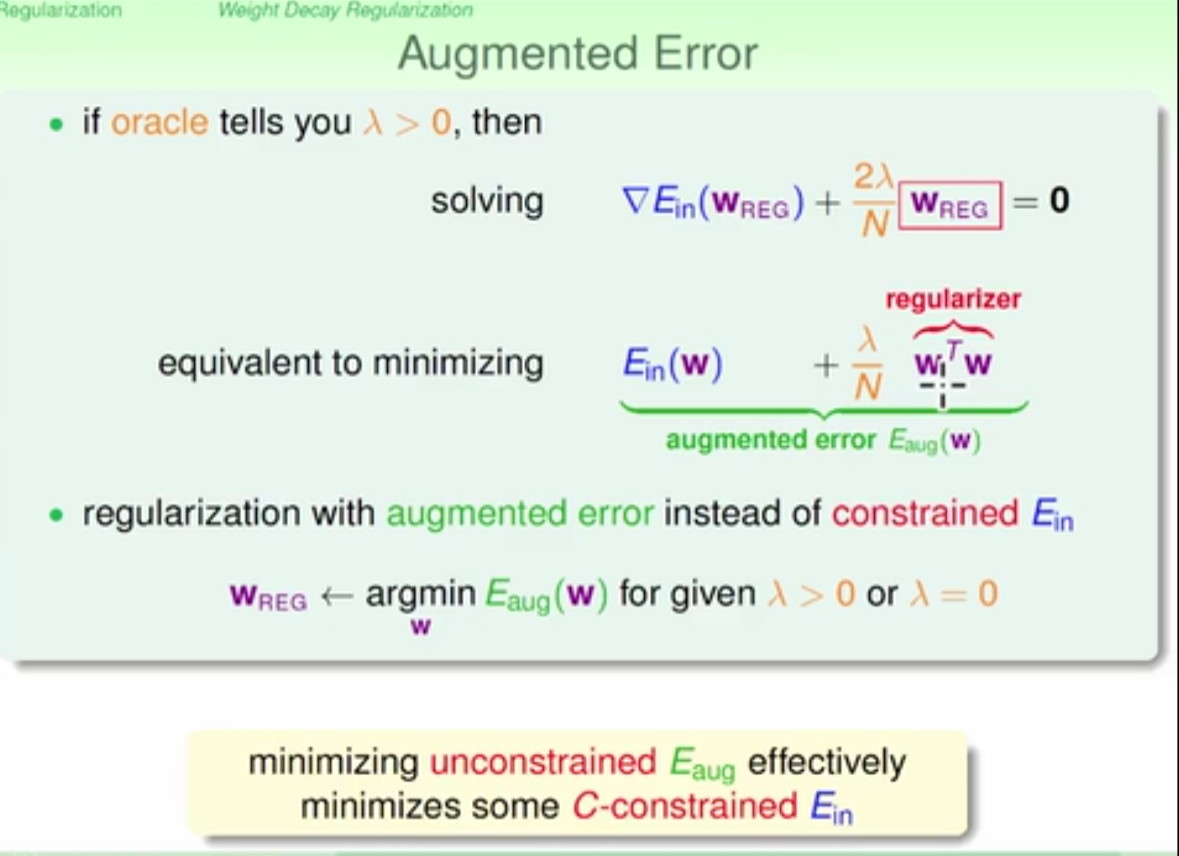

augemented error definition and regularizer definition

regularization prefers smaller lambda and smaller w step during training

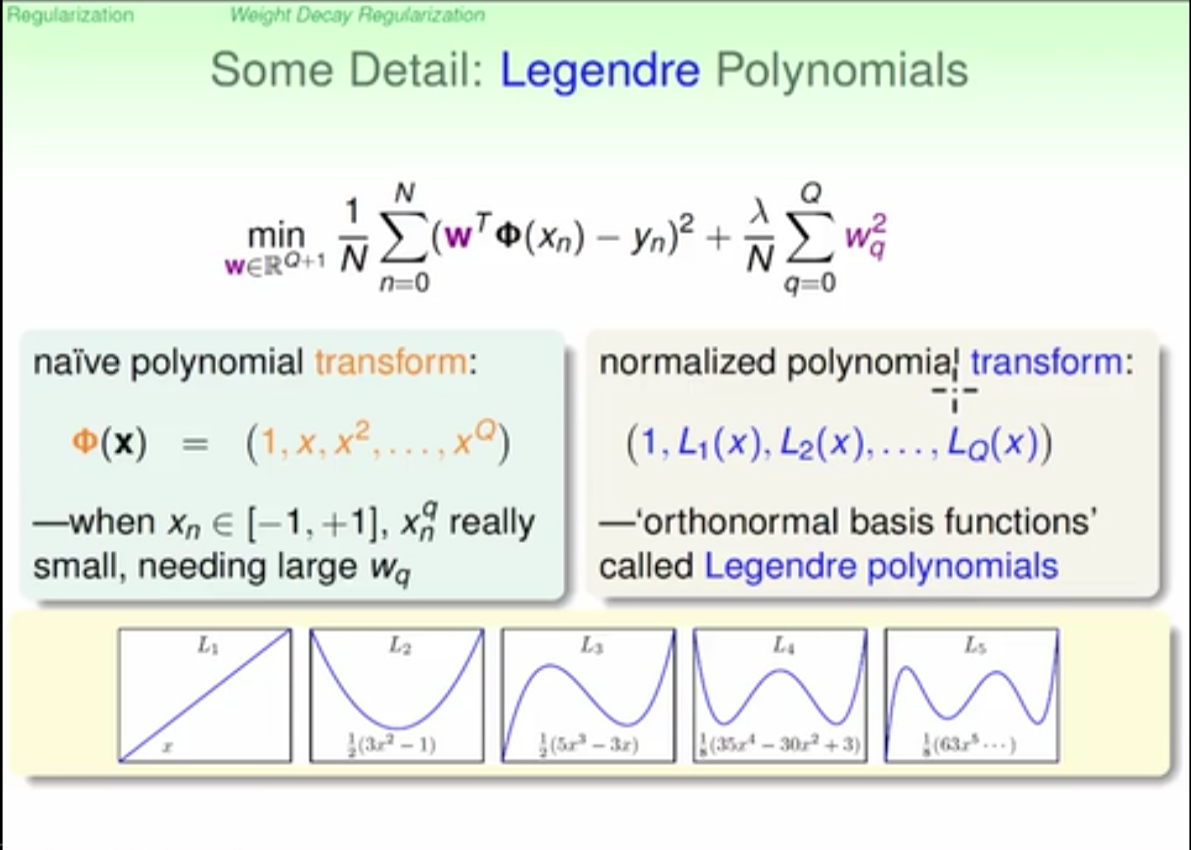

more effective transformation using legendre polynomials than naive polynomials

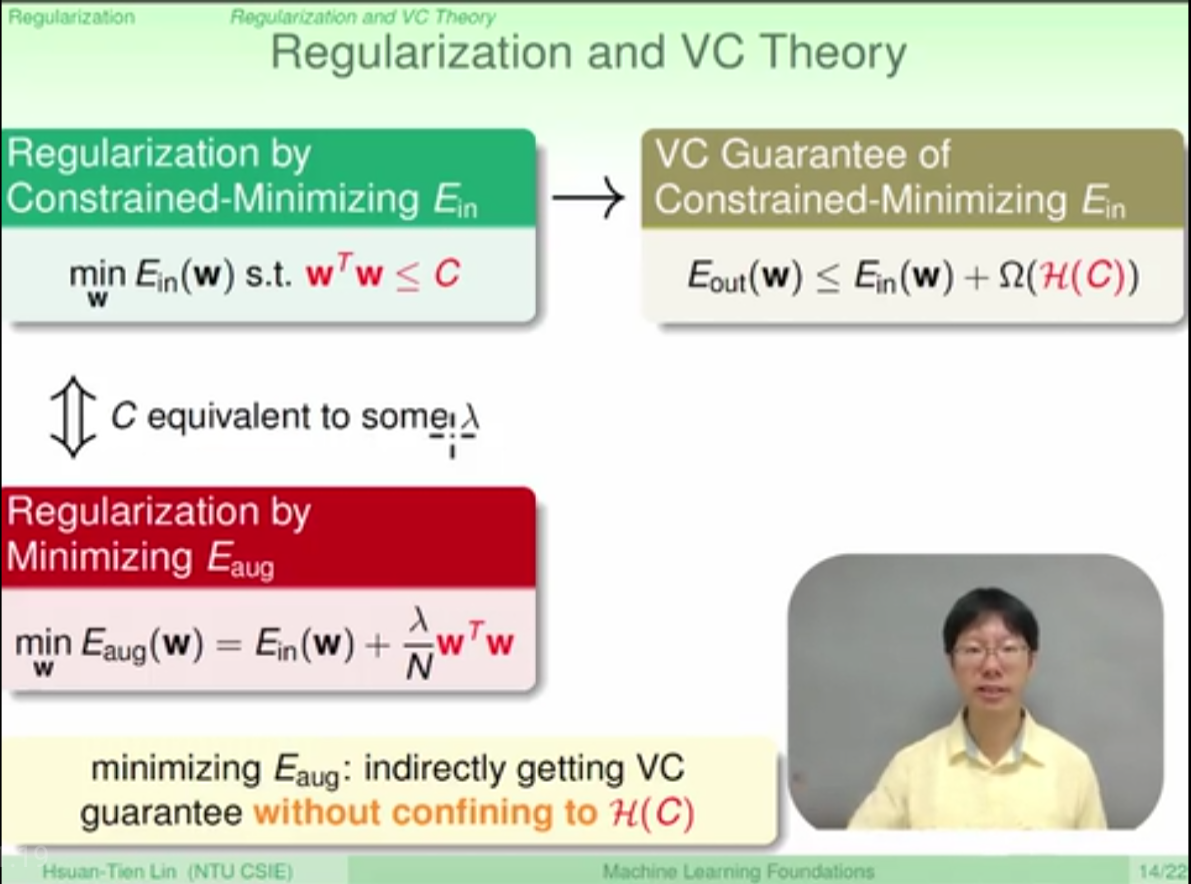

regularization confines to VC guarante with somehow enlarged error range

the model complexity is reduced due to regularization

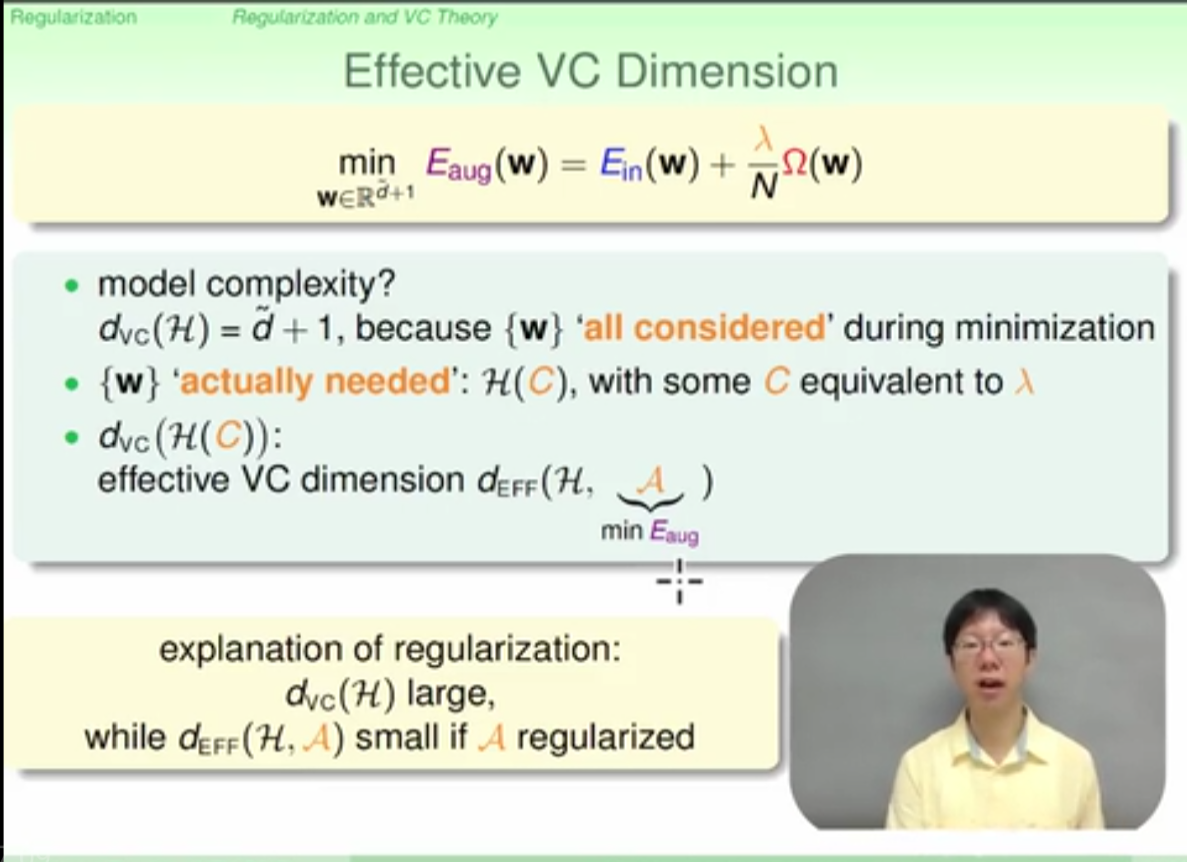

if lambda increases, the effective vc dimension is reduced

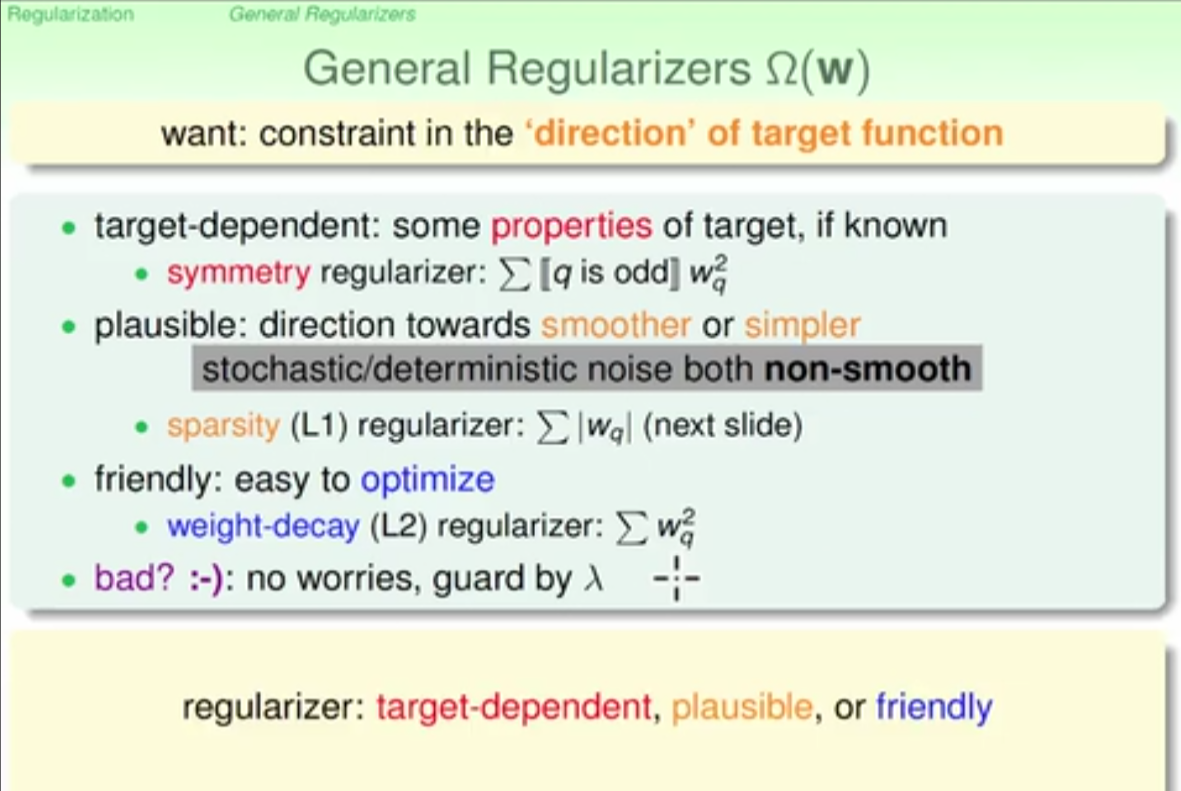

principles to design regularizer:

- target dependent

- plausible

- friendly

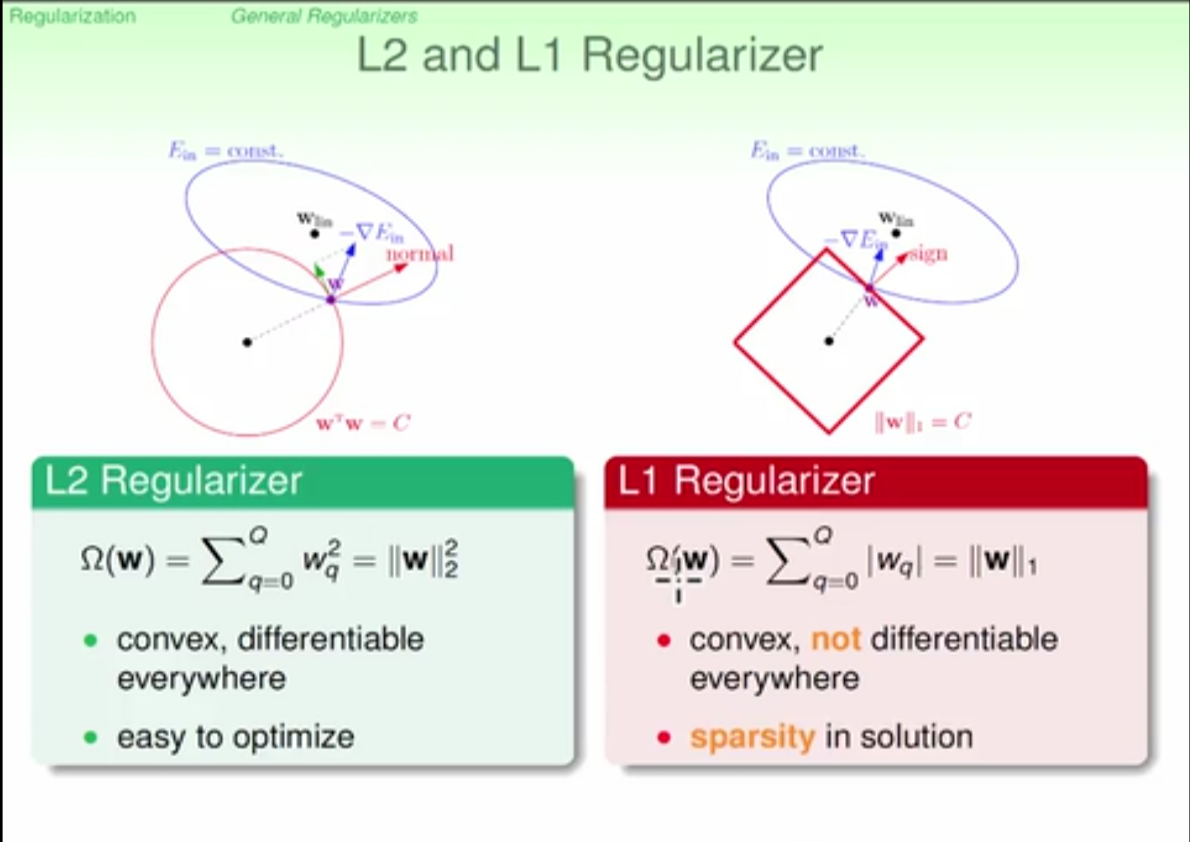

L1 regularizer: time-saving in caculation, solution is sparse but not optimal

L2 regularizer: easy to optimize, precise in solution

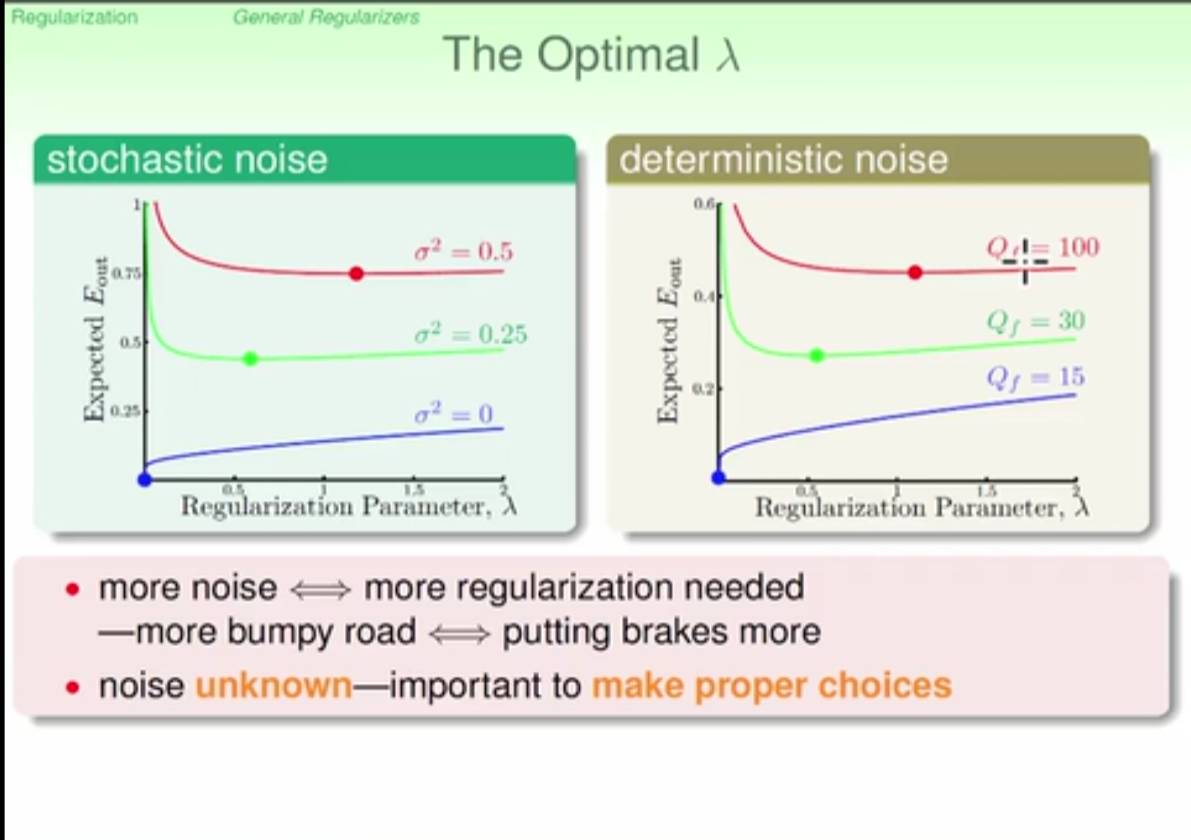

if noise is large then more regularizer is needed

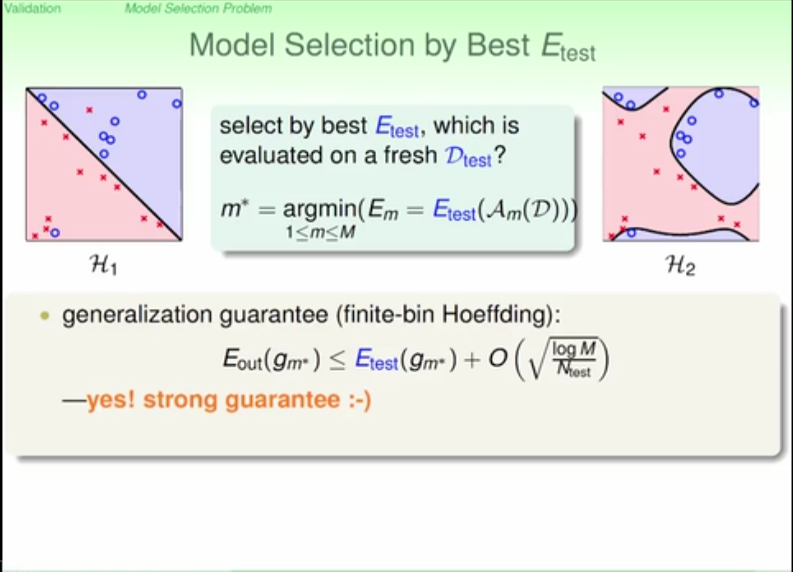

validation

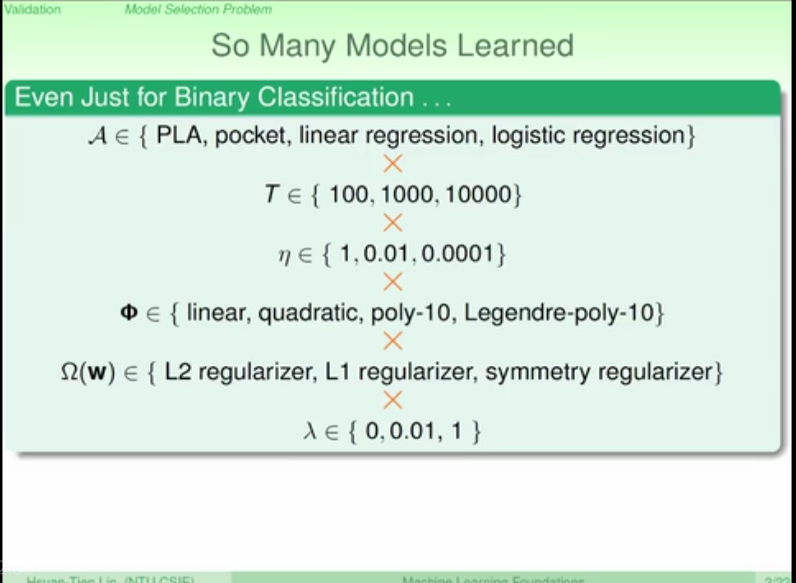

there are lots of hyper-parameters to choose in model selection, all of them are still guaranteed by hoeffdings rule

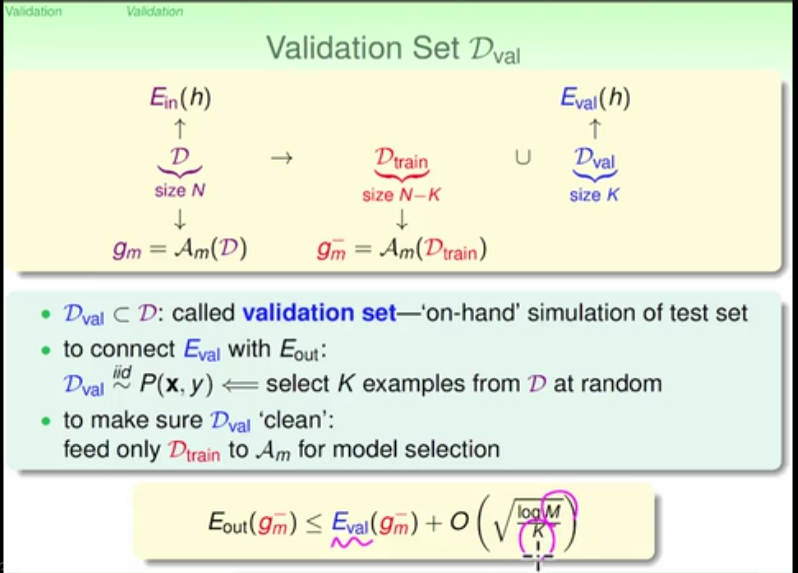

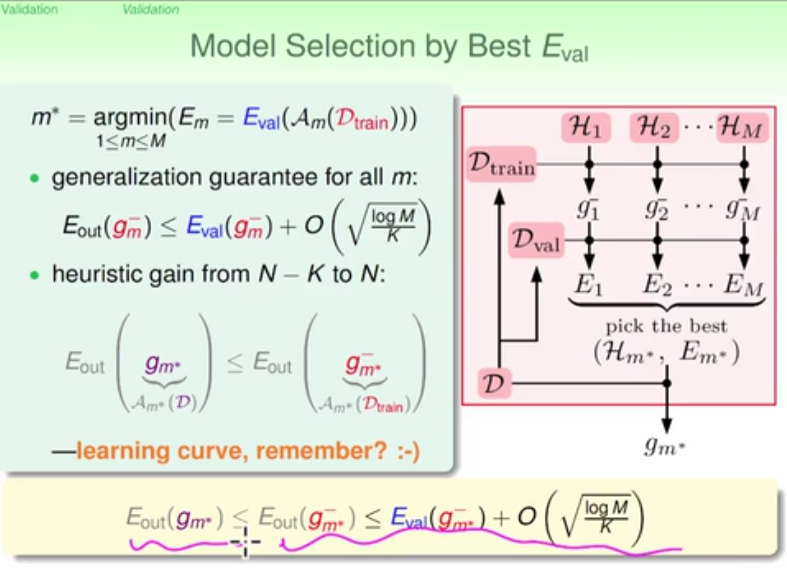

the data set should be divided into training data set and validation data set, validation data set should not be used for training purpose except for cross validation

the traing data set is used to training all modells (g), the validation set is used to select the best modell according to error level

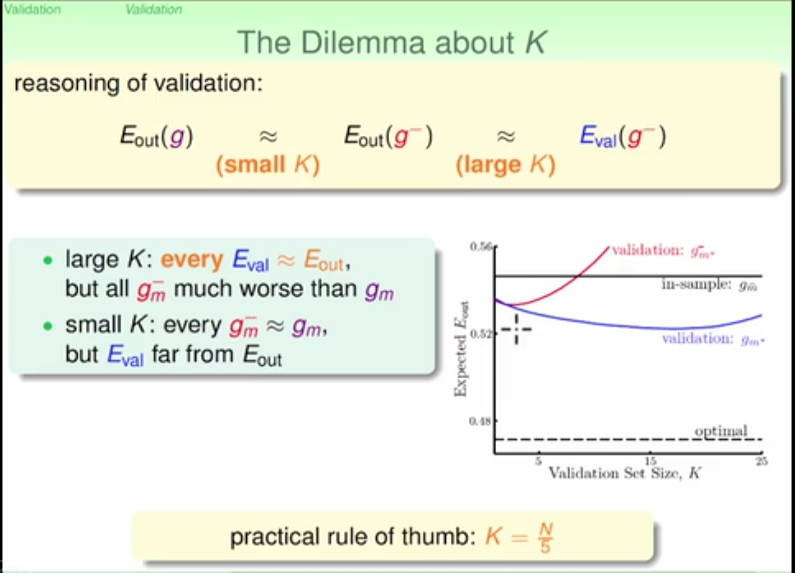

rule of thumb to divide data set into train set and validation set

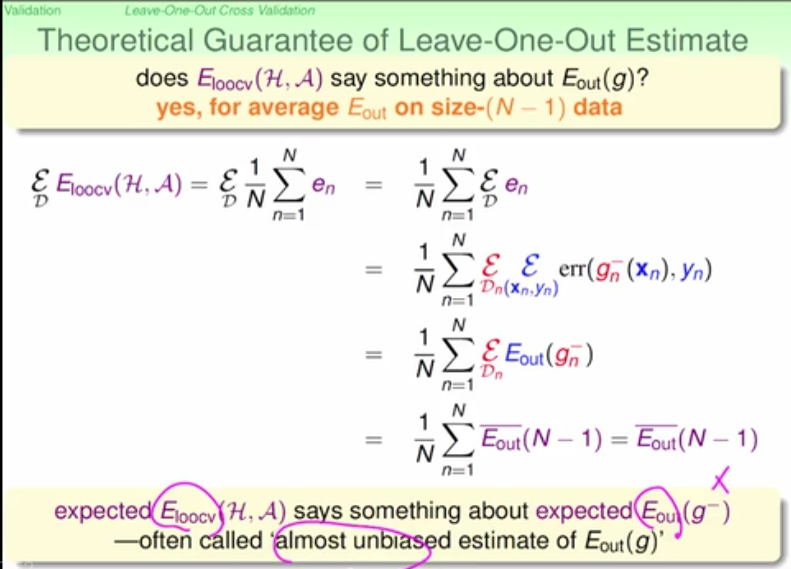

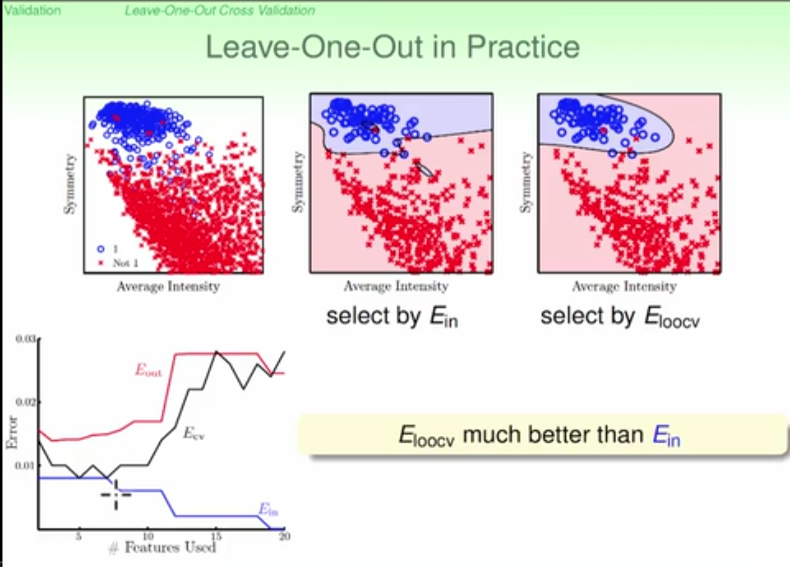

the expected error using validation estimates Eout even better than purely Ein

cross validation:

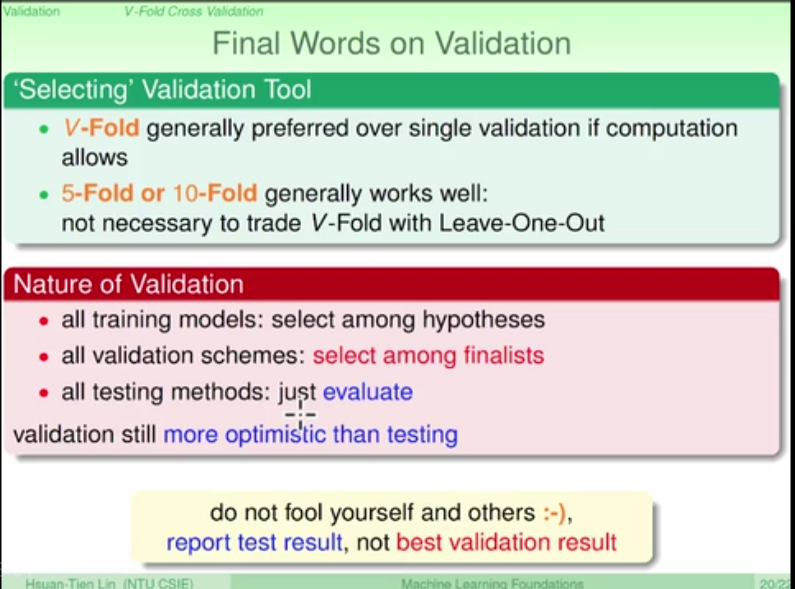

v-fold validation is preferred over single validation if computation allows

5 and 10 fold are good to use

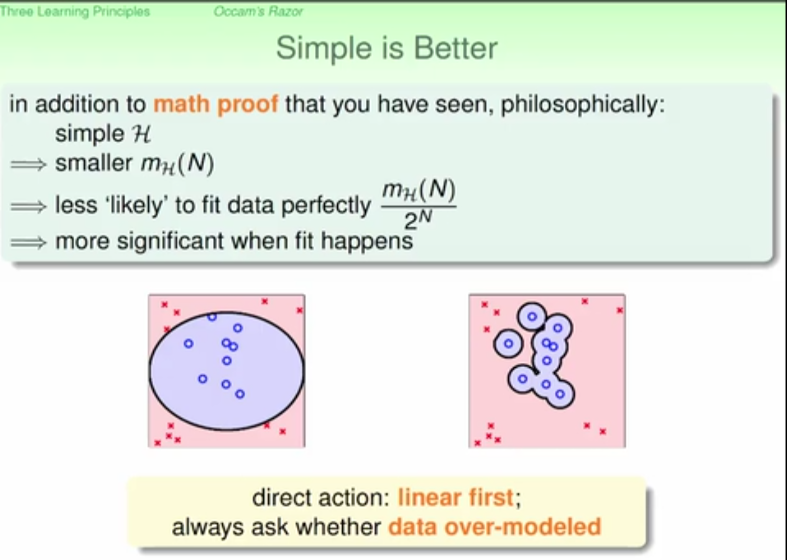

some good suggestions in machine learning

start with simple model to avoid overfit

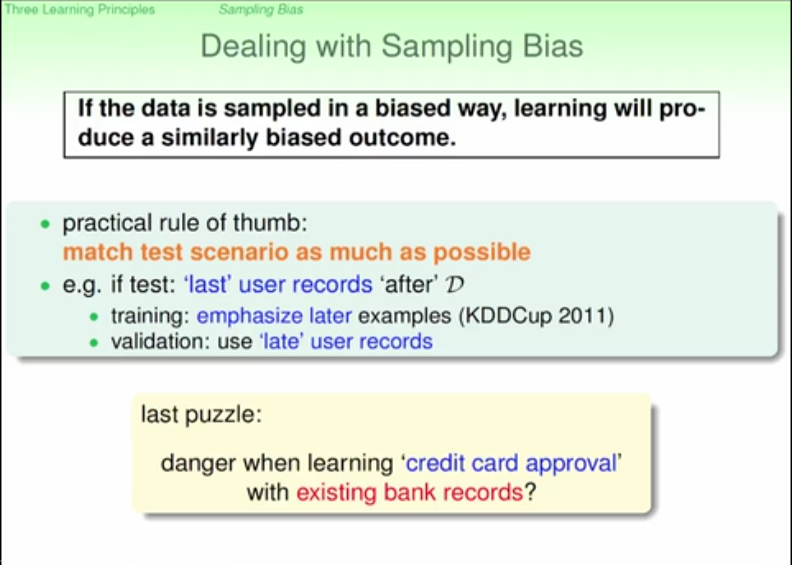

avoid biased data

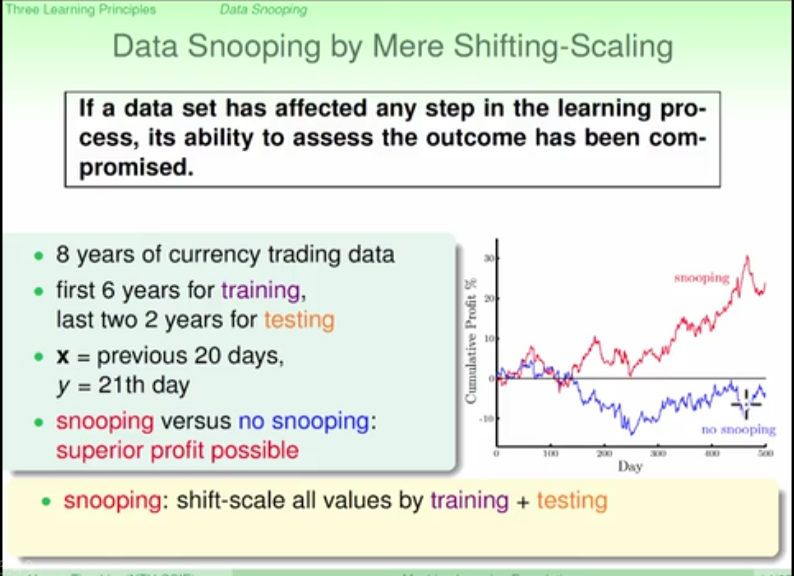

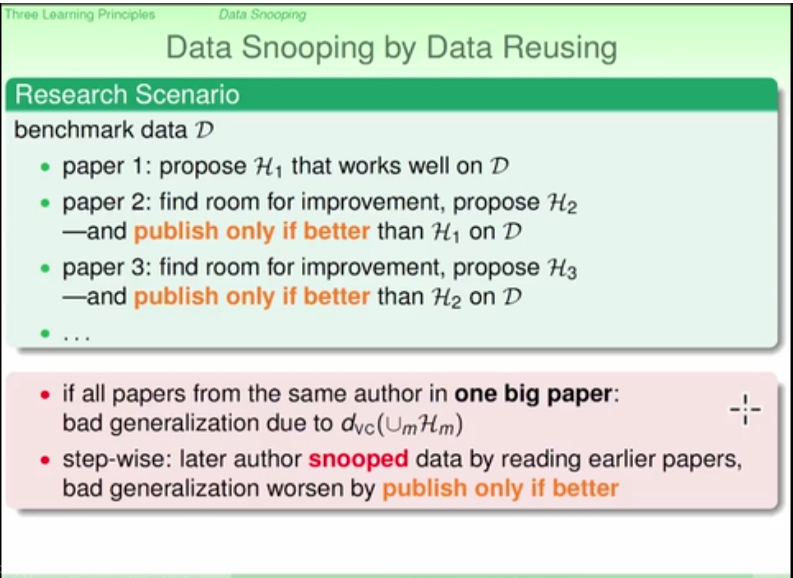

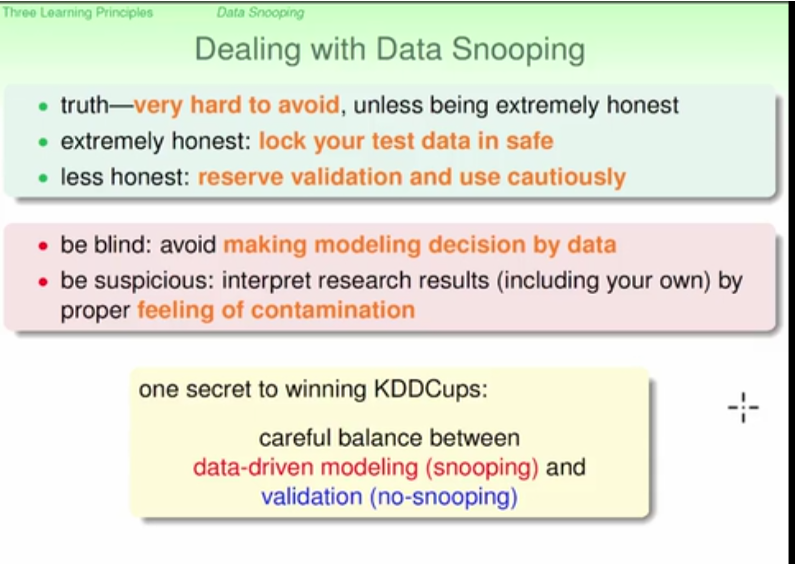

avoid manual data snooping (danger of less generazation)

three learning principles